For most of the past 15-20 years, the market has been flush with cash, and many stocks have traded at astronomical heights without real businesses to support them. In this exuberant market, fundamentals mattered little while momentum and technical rule the day. However, as excess liquidity dries up and global economic concerns weigh on the minds of investors, the reconciliation between cash flows and valuations has arrived. Now, fundamentals matter…a lot. Over the long term, it only makes sense to deploy capital into those businesses that actually generate adequate returns on invested capital (ROIC). Due to change in market mentality, and in light of the recent downturn in the market, we felt it time to revise our price target for Proofpoint (PFPT: $40/share)

Proofpoint’s Business Has Not Improved

We put Proofpoint (PFPT) in the Danger Zone in October 2015. Since then, PFPT is down 33% while the S&P 500 (SPY) is down only 7%. Our report pointed out many problems with Proofpoint, which included:

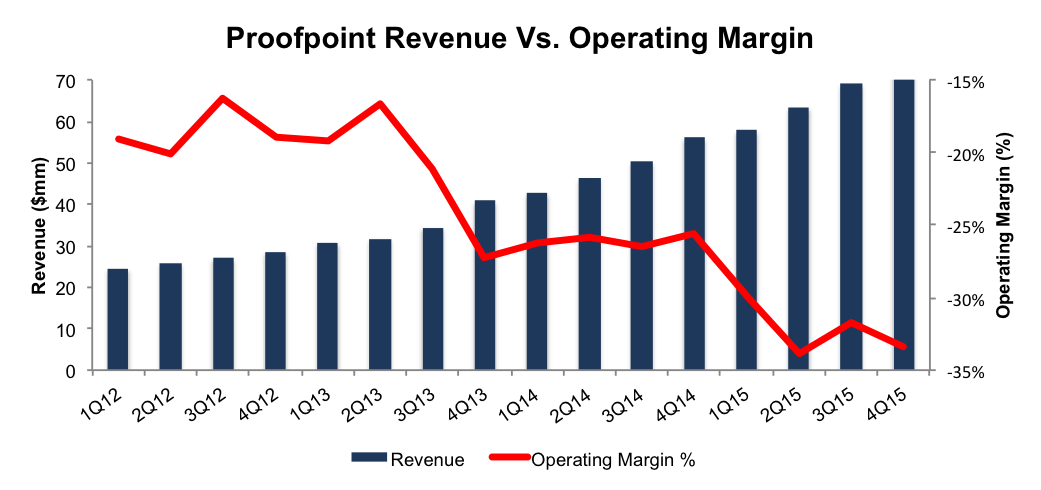

Figure 1 shows that not only is revenue growth slowing, but Proofpoint’s operating margins remain highly negative. Operating margin has fallen from -19% in 1Q12 to -33% in 4Q15. Proofpoint’s after-tax profit (NOPAT) has fallen from -$19 million in 2012 to -$70 million over the last twelve months.

Figure 1: Proofpoint’s Margins Continue To Lag

Sources: New Constructs, LLC and company filings

Ignore Non-GAAP Nonsense

Proofpoint is another company that tries to fool investors with non-GAAP metrics when reporting its results. Despite reporting GAAP net income of -$31 million in 4Q15, Proofpoint reports a positive $573,000 in adjusted EBITDA. How so? Proofpoint removes stock based compensation ($16 million in 4Q15, 22% of revenue), acquisition related expenses, and litigation expenses to help appear profitable when the reality of the business is in stark contrast.

Leave A Comment