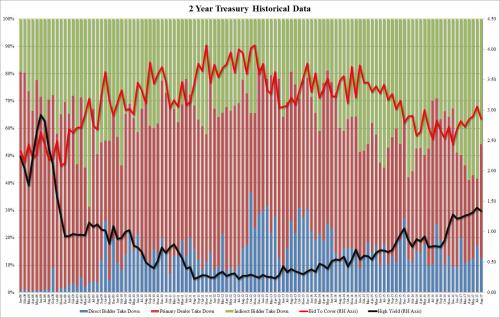

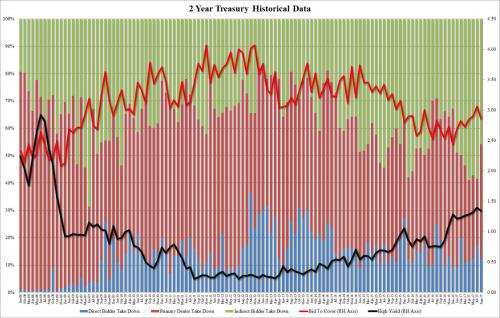

While the high yield of the just priced 2Y auction came “on the screws” at 1.345%, below last month’s 1.401%, but above the six previous auction average of 1.305%. and exactly where the When Issued suggested today’s auction of $26 billion in 2Y notes would price, the internals were decidedly weaker than the stop out would suggest.

The bid-to- cover of 2.86 was a notable decline from last month’s 3.06%, as well as below the 6 month average of 2.90%. It was also the lowest since April.

However, the most surprising aspect of today’s auction was the surprising surge in Dealers take down which surged to 41.6%, up from 24.6% in July, the highest since January, and well above the six auction average of 29.3%. And since the direct bidder award of 12.6% was below both July’s 16.9% award and the six previous auction average 15.0%, it meant foreign buyers, aka Indirect bidders, were awarded only 45.8%, a sharp drop from last month’s 58.5%, and below the six previous auction average 55.7%.

Quoted by Bloomberg, FTN strategist Jim Vogel said that metrics fell short of historical benchmarks due to the “odd timing of the sale and general lack of change in short UST since the end of July.”Bloomberg also notes that the auction was expected to struggle because of U.K. holiday, summer vacations and its position 90 minutes before 5Y issue.

Overall, a rather weak auction which was saved by the jump in Dealer awards, perhaps

Leave A Comment