In an announcement that caught many by surprise, on Monday morning, AT&T said it would acquire Straight Path Communications, a holder of licenses to wireless spectrum, for $1.25 billion in an all-stock deal. The No.2 U.S. carrier said it would offer $95.63 per share, a whopping premium of 162.1% to Straight Path’s Friday close just above $36. This morning, Straight Path’s shares traded as high as $93.26 premarket, up over 150%.

In some ways the announcement should have been expected: Straight Path, one of the largest holders of 28 GHz and 39 GHz millimeter wave spectrum used in mobile communications, said in January it was hiring investment bank Evercore Partners to help explore strategic alternatives, including a sale of assets. The company had also agreed in January to pay the U.S. Federal Communications Commission (FCC) $15 million to settle a federal probe of claims that Straight Path had submitted false data to renew airwave licenses.

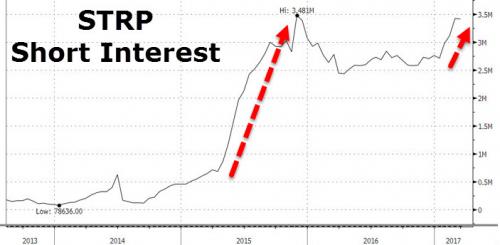

And yet, as the chart of short interest in STRP shows, there were hunders if not thousands of shorts who thought the sale process was a sham. Alas, it was not, and as this morning they are nursing unprecedented pain, not to mention overeager margin clerks.

The short euphoria in the stock was largely due to an ongoing short campaign by prominent short seller, Kerrisdale Capital, which had been waging a long-running campaign against the company, and reiterated as recently as January that it continued to be short. This is what it said in the recent report.

We are short shares of Straight Path Communications, a disgraced “5G” hype vehicle whose stock price surged last week for an unusual reason: the announcement of a harsh regulatory crackdown. After a pseudonymous short seller in 2015 accused Straight Path of “fraud,” the FCC opened its own investigation into whether the company had violated its legal duty to actually provide service rather than merely hoard spectrum for the sake of speculation. To end this investigation, Straight Path agreed to pay up to $100 million over time, surrender many of its licenses, and sell its entire remaining spectrum portfolio, with 20% of the sale proceeds going to the FCC.

The market greeted this news joyously, apparently relieved that Straight Path had avoided an even more draconian penalty and convinced that a spectrum sale would be fast and lucrative. This optimism is badly misplaced. Straight Path’s spectrum is worth far less than the company’s current half-billion-dollar market cap. Indeed, as we discuss below, Verizon is set to buy a similar amount of higher-quality spectrum from a sophisticated, deep-pocketed seller – Carl Icahn – for just $200 million, 61% lower than where Straight Path trades, implying massive downside for its stock price even before taking into account the harsh FCC penalties. Adjusting for these penalties and the lower quality of Straight Path’s spectrum, we believe the true downside exceeds 70%. The notion that a company that holds less than $10 million in cash, burns $7 million a year, and must pay out $15 million in fines in the next nine months will drive a drastically harder bargain than Carl Icahn – in a government-mandated fire sale – is beyond absurd. Yet to own Straight Path at this price, that’s what one must believe.

Leave A Comment