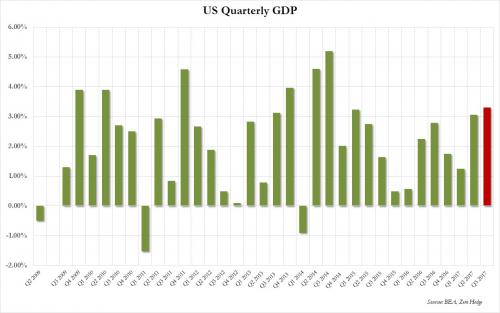

After the BEA estimated that US GDP rose an already impressive 3.0% in Q3, moments ago the Department of Commerce revised its estimate for third-quarter growth to 3.3% annualized, higher than the 3.2% print expected, the highest since the third quarter of 2014.

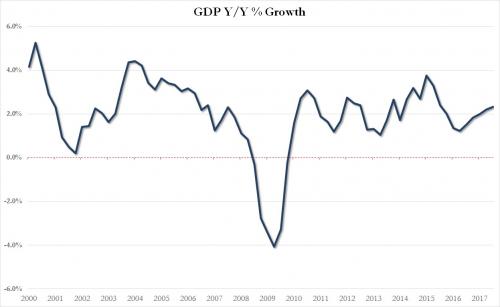

On a Y/Y basis, GDP rose by 2.3%, the highest since Q3 2015:

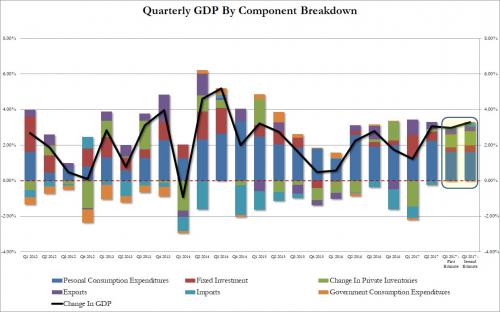

The increase in real GDP reflected increases in consumer spending, inventory investment, business investment, and exports. A notable offset to these increases was a decrease in housing investment. Imports, which are a subtraction from GDP, decreased. The increase in consumer spending reflected increases in spending on both goods and services. The increase in goods was primarilyattributable to motor vehicles. The increase in services primarily reflected increases in health care, financial services and insurance, and recreation services. The increase in inventory investment primarily reflected increases in the manufacturing and wholesale trade industries. The increase in business investment reflected increases in equipment and intellectual property products; these increases were partly offset by a decrease in structures.

Putting numbers to the data, Q3 Consumer Expenditures were revised modestly lower, from contributing 1.62% to the bottom line GDP, to 1.60%. This however was offset by upward revisions to all other GDP components, from Fixed Investment (from 0.25% to 0.39%) and Private Inventories (0.73% to 0.80%), to net trade (from 0.40% to 0.44%) and finally, government consumption, which also rose from -0.02% to 0.07%.

Some other numbers: Core PCE 1.4%, in line with the expected and above 1.3% from the initial estimate. PCE Prices rose 1.5% in Q3, same as consensus and unchanged from the initial estimate. The GDP Deflator came in a little weaker than expected, at 2.1% vs 2.2% exp. That miss however was offset by GDP Sales, which rose from 2.3% in the preliminary report to 2.5%, above the 2.4% expected.

Leave A Comment