The 2016Q3 GDP advance figures were released today, indicating a 2.9% growth rate (SAAR). Tomorrow, Jim will report on the recession probabilities based upon the advance release (see last quarter’s analysis here). Given all the discussion of recession (e.g. [1]), it seems useful to show a few pictures of where we stand today, and the outlook looking forward, given some standard and non-standard indicators.

Here’s the official GDP series and two monthly series.

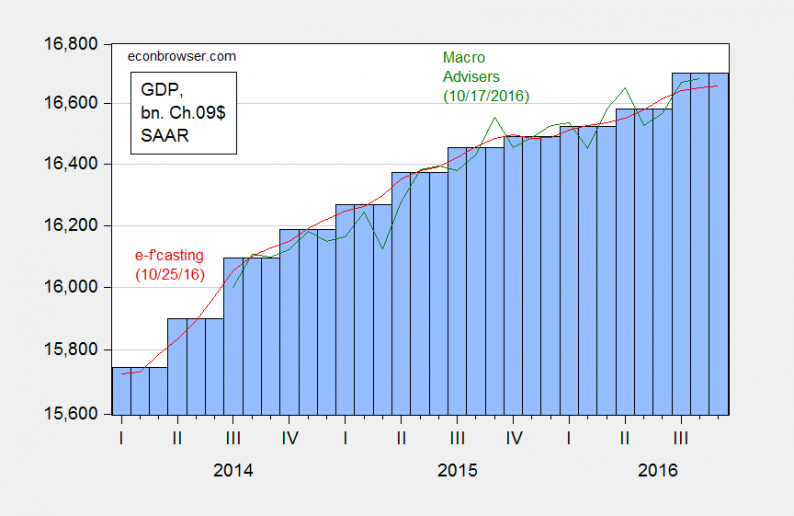

Figure 1: Real GDP in bn. Ch2009$ SAAR, from advance release (blue bar), Macroeconomic Advisers (green), e-forecasting (red). Source: BEA, Macroeconomic Advisers (17 Oct), e-forecasting (25 Oct).

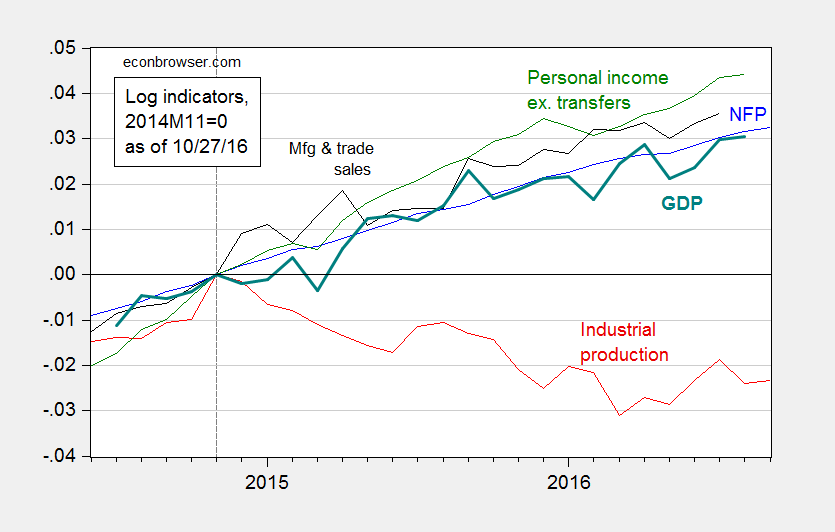

Five key indicators the NBER Business Cycle Dating Committee (BCDC) have in the past examined are depicted below.

All these series continue to rise, save industrial production. As I’ve noted elsewhere, the downturn in manufacturing — ascribable in part due to the strengthening of the dollar and lagging rest-of-world growth — remains cause for concern. Still, this pattern of one indicator declining while others rise is not the same as what occurred in 2008 (see discussion here).

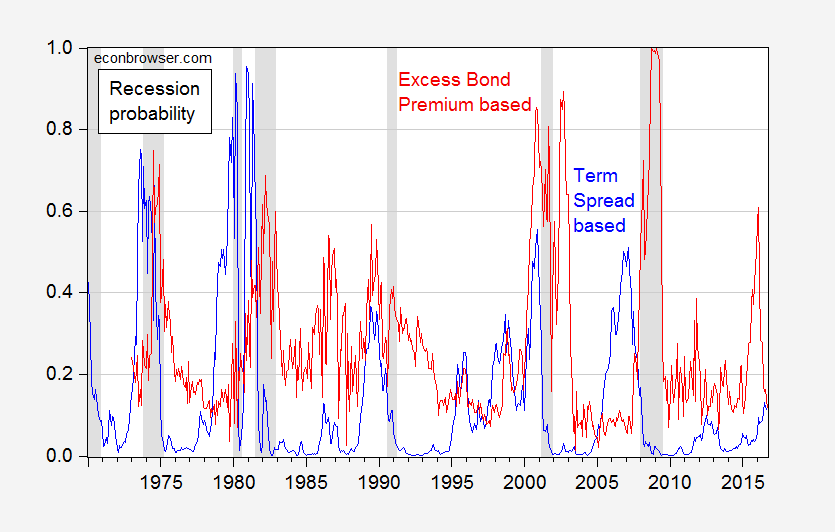

What about the future. Below, I reprise estimates from a term spread model, and one based on the Excess Bond Premium variable defined by Gilchrist and Zakrajšek (2012).

Figure 3: Probability of recession in next twelve months, from term spread (ten year-three month) model (blue), and EBP based (red). Source: Author’s calculations, and Favara, Gilchrist, Lewis, and Zakrajšek (2016).

Given the earlier jump in recession probability using the GZ indicator, it hardly seems time to rest easy. Still, the assessed probabilities as of September are not suggestive of recession in the next year.

Related Posts

Rate-Hike Odds Tumble Post-Minutes; Bonds, Bullion & Black Gold Bid

Rate-Hike Odds Tumble Post-Minutes; Bonds, Bullion & Black Gold Bid Most Important Commodity On The Planet Breaking Last Support Level

Most Important Commodity On The Planet Breaking Last Support Level- Spending Up Far More Than Real Income: Per Capita Income Stagnates

Germany Breaks 9-Year Support, Impact The States?

Germany Breaks 9-Year Support, Impact The States? GBP/USD Forex Signal: Bears Prevail Ahead Of Key UK Data

GBP/USD Forex Signal: Bears Prevail Ahead Of Key UK Data ‘We don’t have much time left’ to regulate crypto, says Bank of France governor

‘We don’t have much time left’ to regulate crypto, says Bank of France governor

Leave A Comment