Retail sales were added in September 2017 due to the hurricanes in Texas and Florida (and the other states less directly impacted). On a monthly, seasonally-adjusted basis, retail sales were up a sharp 1.7% from August. The vast majority of the gain, however, was in the shock jump in gasoline prices. Retail sales at gasoline stations rose nearly 6% month-over-month, so excluding those sales retail sales elsewhere gained a far more modest 0.6%.

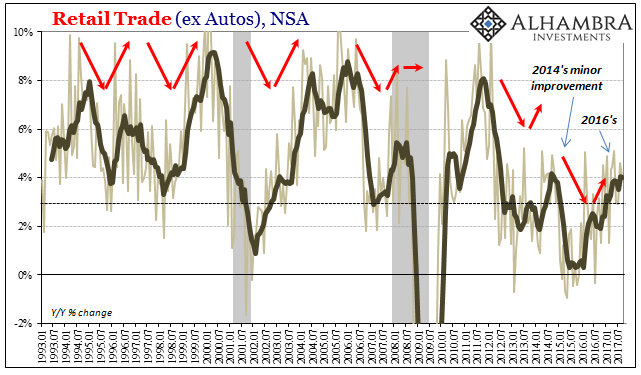

Despite all that, on a yearly basis there wasn’t much effect at all. Unadjusted retail sales in September were just 4.05% more than in September 2016. That compares to a 3.89% rate of growth (revised) in August. It’s the same story repeating; since the 2012 slowdown, a period long enough to be labeled structural, there is a very clear “speed limit” of sorts where even these larger monthly variations don’t do anything to change that.

Six percent growth used to be the level for concern, the lower range of average. Only three times since May 2012 have retail sales been above that level, just slightly so in each case. Of the remaining 61 months, the rate of growth has tended to be around or less than 3%, which is consistent with past recessions (the average rate in those 64 months is just 3.5%).

Because of that, 4% is practically indistinguishable from 3% especially where it is consistently that way – as it has been throughout this year. The 6-month average for retail sales is just less than 4%, not even matching the average gain in 2014 (a year most comparable to the current circumstance).

Excluding gasoline, retail sales year-over-year (NSA) rose by just 3.5%.

There are several reasons to believe that underlying consumer spending is in much worse shape than it may otherwise appear, particularly in the monthly, seasonally-adjusted view. One of the more fascinating and perhaps important marginal shifts over the past almost year and a half has been the sudden appreciation for online shopping (or, more likely, the prices offered via these non-store outlets).

Related Posts

How George Soros Finds His Trades

How George Soros Finds His Trades Indian Indices Trade Marginally Lower; Energy Stocks Witness Losses

Indian Indices Trade Marginally Lower; Energy Stocks Witness Losses Vantiv Inc. – Chart Of The Day

Vantiv Inc. – Chart Of The Day Stocks And Precious Metals Charts – The Court Of The Dragon

Stocks And Precious Metals Charts – The Court Of The Dragon- St. Louis Fed: 60% Of Jobs Automated In Next 20 Years (Spotlight Transportation)

EC

Predictable Non-Residual Seasonality

EC

Predictable Non-Residual Seasonality

Leave A Comment