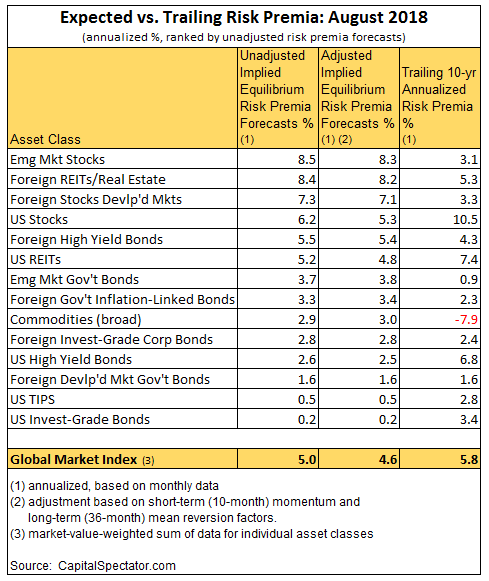

The expected risk premium for the Global Market Index (GMI) continued to inch up in August, reaching an annualized 5.0% — fractionally higher vs. the estimate in the previous month. The projection reflects the annualized return over the estimated “risk-free” rate for the long run for GMI, an unmanaged market-value-weighted portfolio that holds all the major asset classes.

Adjusting for short-term momentum and longer-term mean-reversion factors (defined below) reduces GMI’s ex ante risk premium to an annualized 4.6%, unchanged from July.

Both projections remain moderately below GMI’s historical performance for the trailing 10-year period through last month. The benchmark generated an annualized 5.8% risk premium over the decade through August 2018, comfortably above the current 5.0% expected long-run forecast for GMI.

The forecasting engine for the forward-looking estimates is an equilibrium methodology (defined below) that uses risk (return volatility), the relationship of assets (return correlation), and an assumption of GMI’s expected market pricing of risk (Sharpe ratio) as inputs. The data is based on historical market results starting in December 1997 — the earliest date that offers prices for all the major asset classes (e.g., inflation-indexed Treasuries began trading in the late-1990s). The “risk-free” rate is defined as the yield on zero-to-three-month Treasury bills.

For the underlying market components that comprise GMI, the unadjusted projections for risk premia currently range from a weak 0.2% annualized gain for US investment-grade bonds to a relatively strong 8.5% increase for equities in emerging markets over the long run.

All forecasts are likely to be wrong to some degree, but the projections for GMI are expected to be somewhat more reliable vs. the estimates for the individual asset classes. Predictions for the market components are subject to greater uncertainty compared with aggregating forecasts, a process that may cancel out some of the errors through time.

Related Posts

Trump Eyes Another $267 Billion In Tariffs (And He’s Foolish Enough To Do It)

Trump Eyes Another $267 Billion In Tariffs (And He’s Foolish Enough To Do It) Brexit Impact On British Pound Sterling

Brexit Impact On British Pound Sterling Chinese Trade War Retaliation Sparks Buying Panic In Stocks

Chinese Trade War Retaliation Sparks Buying Panic In Stocks- Price analysis 3/24: BTC, ETH, BNB, XRP, ADA, DOGE, MATIC, SOL, DOT, LTC

Is Bitcoin Really A Leading Indicator For The Entire Market?

Is Bitcoin Really A Leading Indicator For The Entire Market? GBP/JPY Low Volatility Zone Breakout Spikes The Price

GBP/JPY Low Volatility Zone Breakout Spikes The Price

Leave A Comment