Previously we documented that as a result of the still low oil prices, largely a result of Saudi Arabian strategy to put high cost producers out of business and to remove excess supply, none other than Saudi Arabia has been substantially impacted, with the result being dramatic state budget, a sharp economic slowdown and mass worker layoffs.

Just three weeks ago we reported that the biggest construction conglomerate in the middle east, the Saudi Binladin Group had announced it would layoff 50,000 workers ot a quarter of its workforce, slammed by the weak economy.

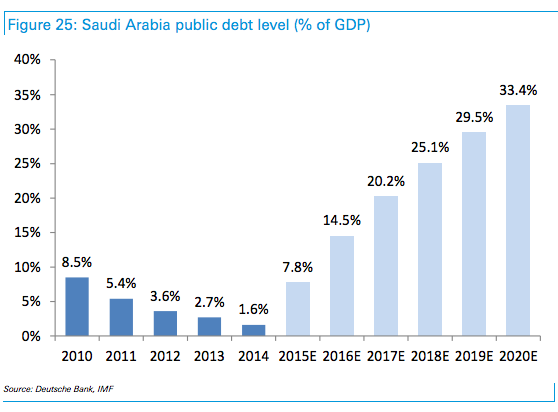

Now, Saudi Arabia has admitted that in addition to acute economic problems, which will manifest themselves most directly in a soaring Saudi debt load…

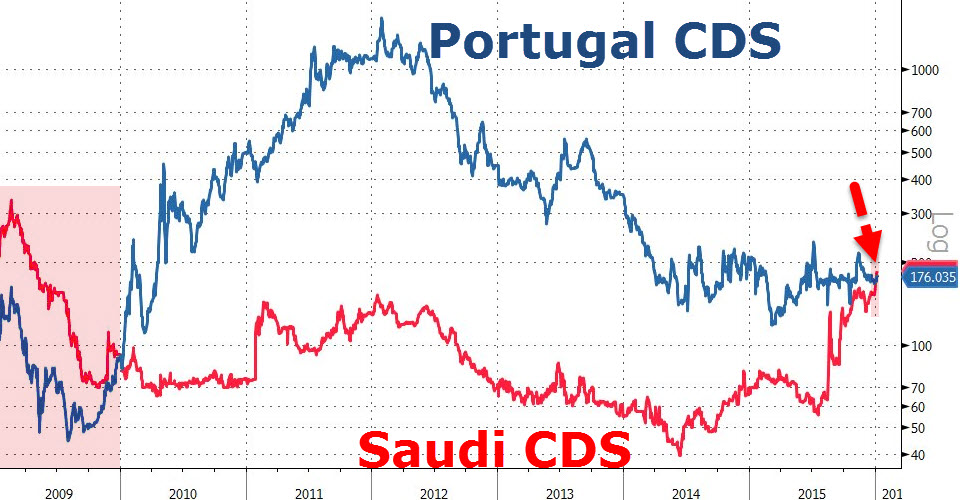

… and rising default risk…

… Saudi Arabia can also add liquidity worries which just spilled out into the open, because Bloomberg reported moments ago, Saudi Arabia has told banks it is considering paying some outstanding bills to contractors with government-issued bonds, citing people with knowledge of matter say.

Contractors would be able to hold bond-like instruments until maturity.

Bloomberg adds that issuing bonds is one of several options being considered.

Contractors so far received some payments of outstanding bills from government in cash.

Saudi Arabia’s finance ministry declines to comment, while central bank didn’t immediately return calls seeking comment

What this means is simple: as a result of the budget imbalance driven by low oil prices, largely a Saudi doing, the kingdom is forced to give workers an implicit pay cut. It also means that since the government has to “pay” through the issuance of debt, that the liquidity crisis in the kingdom is far worse than many had anticipated.

Which brings up the question of devaluation: how long until the SAR has to follow the Yuan and see a substantial haircut. According to the market, 12 month SAR forward are now trading at a price which implies a 12% devaluation in the coming months.

Leave A Comment