At the end of February, FRBNY President Bill Dudley made what was a widely shared remark that “animal spirits had been unleashed.” Confidence of just this sort is exactly what monetary policy is after, using all kinds of tools by which to get people happy about the future. According to rational expectations theory, which guides every post-Great Inflation model, if people feel tomorrow will be better and are very confident about that feeling, then they will act today in anticipation. It’s not monetary policy without money so much as pop psychology.

The job of the Federal Reserve through this channel sounds really simple – provide these “animal spirits” with a credible, plausible basis by which to be sustained and amplified. From stocks to inflation expectations, the QE’s were supposed to instill this kind of foundation for full recovery.

Dudley’s comments six weeks ago, however, were not in relation to QE but rather the election. In that way, his remarks were almost damning of monetary policy because the world at the time looked a lot brighter for reasons that had little to do with him or the FOMC. But this was not the first time confidence and spirits had been unleashed, for the same could have been said, and was, about 2014 and early 2015 (which were attributed to the success of QE and its presumed positive boost in confidence).

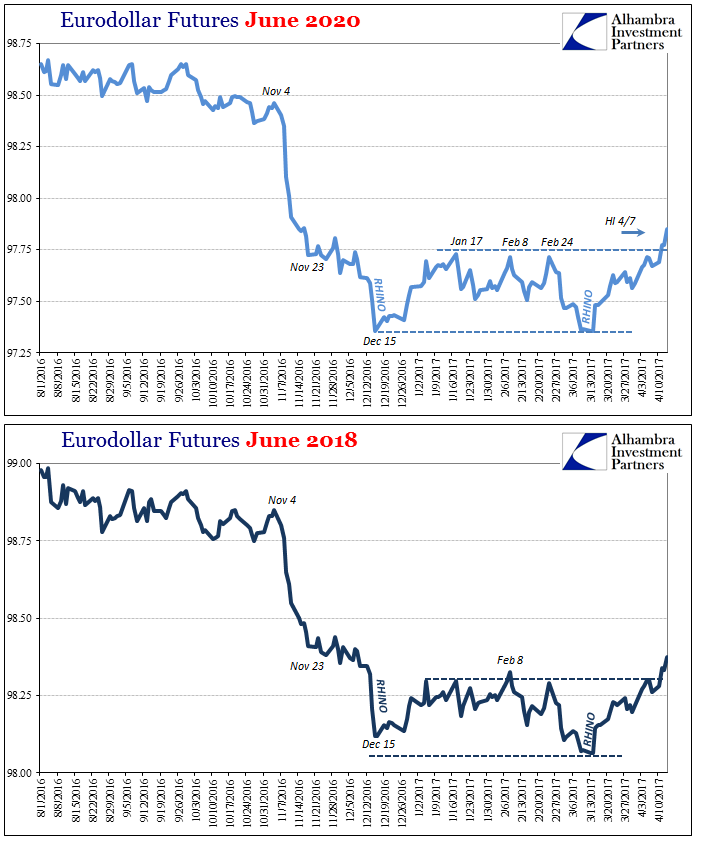

Yet, ever since the Fed last “raised rates” in mid-March it’s as if the whole thing fell apart. From almost the moment the FOMC published its “hawkish” vote, risk aversion has been the dominant force once again. It is contrary to everything we are supposed to believe about monetary policy and what it means under these conditions. As Reuters wrote back on March 16, a good representation of convention “wisdom” about these things:

The U.S. Federal Reserve raised interest rates on Wednesday for the second time in three months, a move spurred by steady economic growth, strong job gains and confidence that inflation is rising to the central bank’s target.

There is supposed to be a robust relationship between monetary policy, inflation expectations, confidence, and then inflation and output. That is what “accommodation” means, and the end of “accommodation” therefore must mean the confidence stage is finally turning into the activity stage; animal spirits progressing from confidence into actual inflation and activity.

Related Posts

HH

Gold Stocks – Update On A Tricky Situation

HH

Gold Stocks – Update On A Tricky Situation WTI Crude Oil And Natural Gas Forecast – Wednesday, July 5

WTI Crude Oil And Natural Gas Forecast – Wednesday, July 5 Merck & Co. Inc Shares Fly High On Positive Lung Cancer Trial

Merck & Co. Inc Shares Fly High On Positive Lung Cancer Trial Crypto exchange Roqqu receives South African approval to expand operations

Crypto exchange Roqqu receives South African approval to expand operations Difficult Market Spooks Investors

Difficult Market Spooks Investors- The U.S. Government Massive One-Day Debt Increase Impact On Interest Expense & Silver ETF

Leave A Comment