Despite the bearish start to the week on Monday and a bearish initial response to Friday morning’s employment report for September, the bulls managed to reversal course Friday afternoon to hammer out a big gain for that day and even a small gain for the week. A couple of the key indices even managed to climb back above their short-term moving average lines.

There’s still work to be done — from both sides of the table — if we’re ever going to get out of this rut. But, a bullish break out of the rut is once again a possibility.

We’ll paint a picture of it below, after running down last week’s and this week’s major economic announcements.

Economic Data

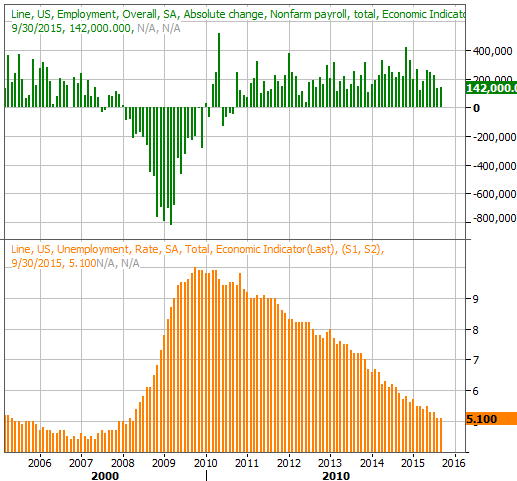

Last week’s economic dance-card was plenty full, but the highlight of the week was the grand finale… September’s unemployment data, unveiled on Friday. The unemployment rate held steady at 5.1%, even though payroll-creation slowed to 142,000. July’s and August’s job-growth numbers were also revised in a downward direction.

Employment Growth, Unemployment Rate Chart

Source: Thomas Reuters

It’s also worth mentioning hourly wage growth was stagnant last month.

The data is a bit of a double-edged sword. On the one hand it’s alarming to see job-growth slow down, as is suggests economic growth is stalling. On the other hand, it gives the Federal Reserve time, room, and reason to postpone any rate hike that was in the cards. The odds were still technically favoring a March hike rather than a December hike, but the odds of March being the month it begins were raised even further on Friday.

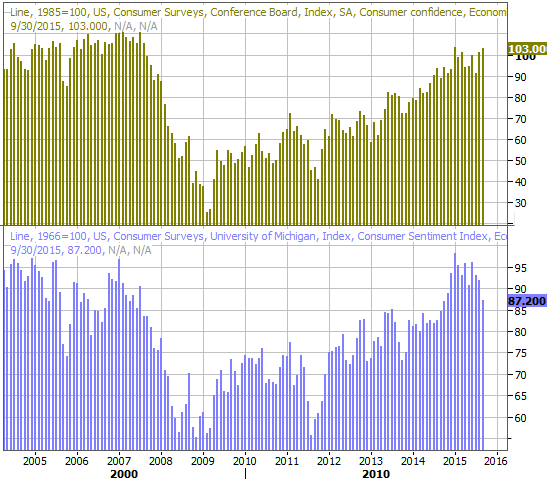

We also heard September’s consumer confidence (Conference Board) score last week. Amazingly enough – and despite the fact that the Michigan Sentiment Index score fell – consumer confidence jumped from 101.3 to 103.0, whereas economists were looking for a decline.

Consumer Confidence, Sentiment Chart

Source: Thomas Reuters

Everything else is on the following grid:

Leave A Comment