Will U.S. Economy Remain Stable as Interest Rates Soar?

Interest rates in the United States are skyrocketing. This could mean a lot of trouble ahead for corporate America and American consumers.

Too often, everyone gets boggled by the rates set by the Federal Reserve, the federal funds rate (FFR). It’s the most basic interest rate, but it’s not the rate that the average business or consumer gets for a loan or mortgage. The FFR is just for the banks.

To get a better idea of interest rates for businesses and consumers, it’s important to pay close attention to the yields on U.S. bonds. Sadly, as it stands, those interest rates are just soaring.

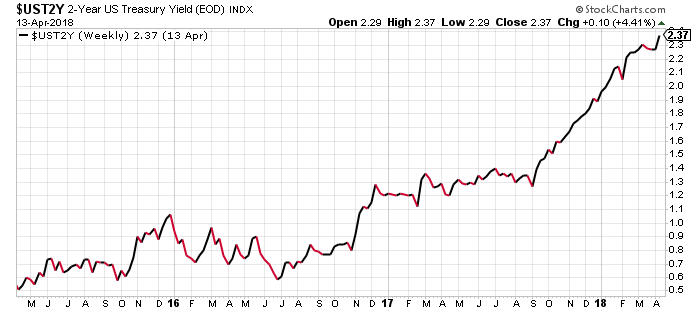

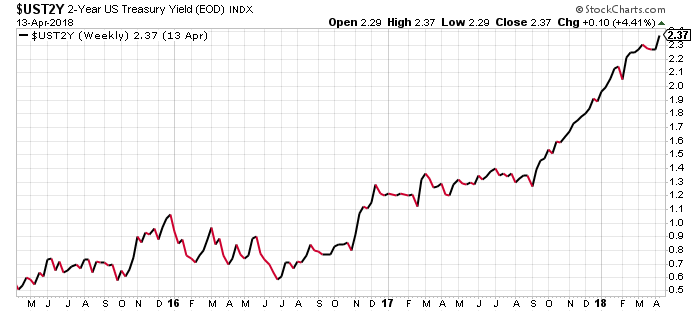

Look at the chart below, for example. It shows the yield on the two-year U.S. Treasury.

Chart courtesy of StockCharts.com

In mid-2015, yields on the two-year U.S. Treasury was around 0.2%. Now it’s 2.37%. That’s an increase of close to 1,100% in matter of just few years. The yields on these U.S. bonds stand at the highest level since the 2008 financial crisis. Since mid-2017, they have seen an almost vertical increase to the upside.

Why bother paying attention to the yields on the two-year U.S. Treasury? A business may get a short-term loan based on this rate. In June 2015, the business could have been paying just $0.20 on every $100 they borrowed. Now it’s $2.37.

Businesses in the U.S., all of a sudden, could be incurring much more interest expense than they did just three years ago. Remember this: interest rates directly impact profitability. The higher the interest expense, the lower the profitability.

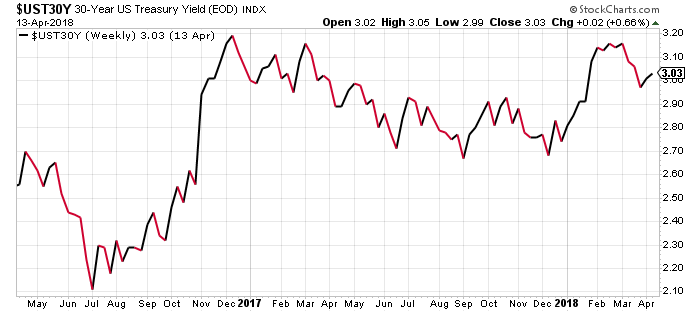

Mortgage Rates Soar as 30-Year Bond Yields Surge

But don’t just stop here; look at the yields on the 30-year U.S. Treasury.

Chart courtesy of StockCharts.com

In mid-2016, yields on the 30-year U.S. Treasury was 2.1%. Now it’s 3.03%. This represents an increase of 44.3%.

Why does the 30-year U.S. Treasury yield matter? Long-term mortgage rates usually move in a similar direction as the yields on 30-year U.S. bonds.

Related Posts

The new digital, decentralized economy needs academic validation

The new digital, decentralized economy needs academic validation July Jobs Report: Booming Jobs Market, And A Surge In Participation Continues To Depress Wage Growth

July Jobs Report: Booming Jobs Market, And A Surge In Participation Continues To Depress Wage Growth- Buying Options Into Apple’s Earnings

The 57 Startups That Became Unicorns In 2017

The 57 Startups That Became Unicorns In 2017 This platform makes transfers cheaper, opens access to digital assets, and protects consumers

This platform makes transfers cheaper, opens access to digital assets, and protects consumers How smart regulation can improve the future of blockchain

How smart regulation can improve the future of blockchain

Leave A Comment