Now that even permabulls are openly discussing a recession as a possibility for the US economy, a comparable and far more dire scenario is making the mainstream rounds: a China hard-landing.

Earlier today, SocGen decided to model out what what would happen to equities in just such a scenario. In fact, it took it one step further and combined this with what an “EM lost decade”, one which increasingly looks more realistic, would look like.

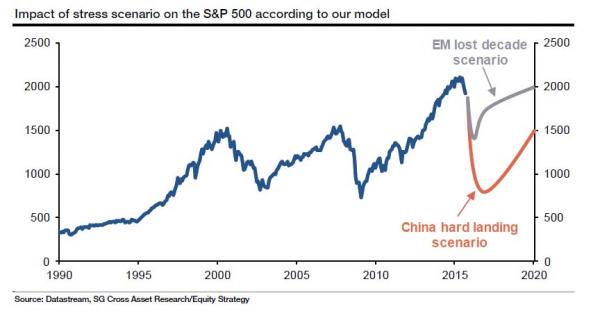

This is what it found:

Our model indicates the US equity market could potentially drop by 30% in the event of an ‘EM lost decade’ and by 60% in the event of a China hard landing (i.e. S&P 500 back to its lows).

The silver lining will depend on just how aggressive the response to such a collapse will be:

The amplitude of the correction would be a function of the policy response. In both scenarios, we think global equities would rebound strongly after

having overshot (i.e. equities to price in a more optimistic scenario).

SocGen then provides the following seven investment recommendations for what would be more or less an apocalypse for risk assets:

While the above are largely self-exlanatory, SocGen adds the following explainer:

The 2015 summer sell-off highlighted how nervous the markets are regarding any risk coming from China: the S&P 500 index lost 11% in one week, the Eurostoxx 50 fell 16% and the Nikkei was down 13%. Whatever the scenario (hard landing or EM lost decade), if China’s GDP growth were to drop by c. 2% between 2015 and 2016, volatility would jump and the equity market would price in a lack of future growth (i.e. via a spike in the risk premium).

And some more details:

‘EM lost decade’ scenario: a square root-shaped equity market

Stressing our equity risk premium model indicates that the S&P 500 could potentially drop by 30% to 1400pts due to a strong move in the risk premium during 2016. In such a scenario, the market could quickly rebound (by year-end 2016) in line with commodity prices. We would expect support from central banks and the resilience of the US and European economies to support developed equity markets, which should gradually recover, albeit to a lower level. We thus imagine a square root-shaped scenario in which European equities would underperform US equities, but would then rebound stronger (on the back of a lower oil price, weaker currency, a more aggressive ECB and more attractive valuations).

‘Chinese hard-landing’ scenario: a V-shaped equity market trend

In our hard-landing scenario, a theoretical drop in China’s GDP growth from 6.9% in 2015 to 3.0% in 2016 and its consequences would have a major impact on global corporate earnings. We would expect a sharp sell-off of global equities in such a scenario. Our risk premium model indicates that the S&P 500 could in theory return to its lows (around 800pts). But then again the deflationist shock could prompt the central banks to turn more aggressive and support the equity markets to prevent the S&P 500 from sliding into such a bear market. We think that after such a shock the global equity market would rebound strongly on a return to growth in China and central banks actions.

Leave A Comment