Oil prices have bounced back a lot, despite recent softer price action that sees crude near $60.

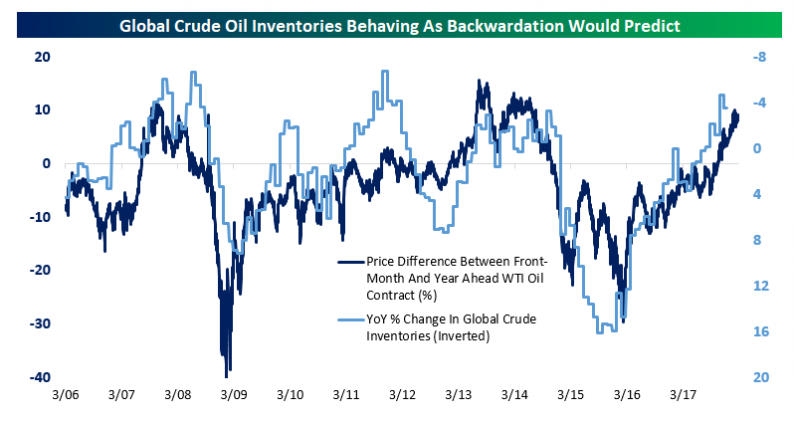

That’s put near-month crude at a hefty premium to out-months, a so-called backwardation of the WTI curve. As shown in the chart below, the ~10% premium for front-month over year-ahead crude is about as high as it’s gotten over the past decade or so. The price differential provides a huge incentive for investors to supply crude to the market by selling spot crude and buying out-months. That creates a positive yield.

The opposite was true in the period when the WTI curve was in contango; investors had an incentive to buy spot and sell out-months, driving up inventories. As shown in the chart below, while inventories and the shape of the crude curve are not perfectly correlated, they’ve got a very close relationship. As long as out-months remain at a discount to the front of the curve, don’t be surprised to see global stockpiles continue to shrink.

Related Posts

Gold’s Fundamentals Are Not Bullish…Yet

Gold’s Fundamentals Are Not Bullish…Yet Investors Beginning To Embrace Risk

Investors Beginning To Embrace Risk The Cost Of China’s “Manipulated Market Stability” May Be Too High, BofAML Warns

The Cost Of China’s “Manipulated Market Stability” May Be Too High, BofAML Warns Swiss Franc Plunges To One-Year Lows Amid SNB Intervention Chatter

Swiss Franc Plunges To One-Year Lows Amid SNB Intervention Chatter Migration From A Global Perspective

Migration From A Global Perspective- The Opening Of The American Macroeconomy And The Implications For Monetary Policy

Leave A Comment