In the past few years stock buybacks have been increasingly criticized by investors who believe the stock market and economy are in a bubble. The main evidence they bring to the table is that companies bought back a record amount of their own shares before the financial crisis in 2008. The market fell about 55% in 2008, thus making the stock buybacks poorly timed. Furthermore, some firms issued shares at the suppressed low prices following the crash due to liquidity issues. However, this is a poor argument against buybacks because there was also high capex spending and elevated M&A activity before the recession. M&A activity and capex also usually peak before recessions as the economy is thriving and capital is flowing.

Expensive Acquisitions & Exaggerated Potential Cost Savings

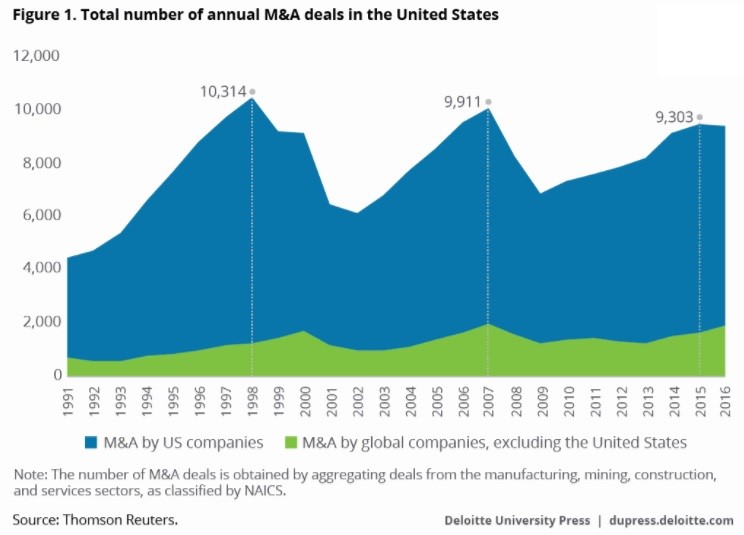

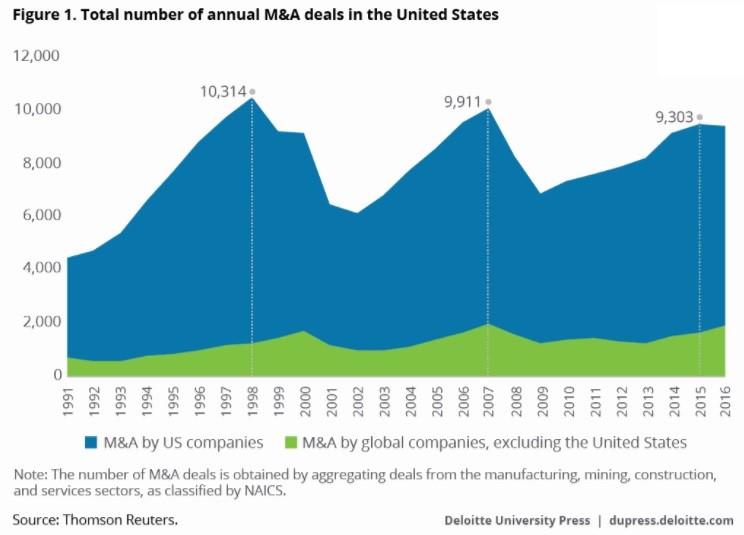

As you can see from the chart below, the number of M&A deals peaked in 1998 which was 3 years before the recession and 2 years before the stock market peak.

History Of M&A Deals

The total deals reached a high in 2007 which was the year the stock market peaked and when the recession started. If valuations are high and the economy is about to crater, no matter where a firm puts the money, it will look like a poor investment in a few years. It seems more rational to return the capital to shareholders through dividends and buybacks instead of making an expensive acquisition, which can cause a company to take on excessive leverage that would devastate it during a recession. When acquisitions are made, the cost savings, commonly referred to as “synergies”, are often overly inflated, especially when the businesses aren’t similar. Shareholders can correctly criticize an acquisition if they think it could have been cheaper to get into that new line of business and grow a product organically. A shareholder can’t rationally get mad at a company for buybacks since if you own the stock, you must think it is undervalued which means buybacks make sense – otherwise, you would sell the stock. Stock buybacks are also the tax efficient way to return capital to shareholders compared to dividends which are not tax efficient.

Leave A Comment