The initial recovery off last week’s lows (near Dow 25K) was short-lived, quickly fizzling out ahead of Dow 26K, a key technical retracement. Once a former region of support turned resistance was highlighted, short-term momentum had quickly shifted back to equity bears, allowing for the latest bout of negativity to carry over into this week’s price action. This eventually led the Dow (DJIA) to gap lower this past Tuesday near the psychological 25K region, which managed to keep bumpy price-action nearby before closing just below the threshold on late Thursday.

The earnings disappointment overnight, by the two of the largest companies in the world (namely Alphabet & Amazon), not only put pressure on the technology sector but added near-term technical risks on all equity markets. More specifically, it puts the Dow in position to start trending lower towards the summer’s lows near 24K while counter-rallies remain south of 25K and the 200-day Moving Average (near 25K). Friday’s intra-day high briefly probed the October 11th swing low (24,899.70), which also hints that bears remain in control until bulls reclaim 25K and/or the 200-day MA on a daily closing basis.

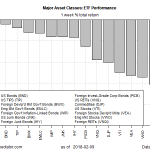

Wild swings in the market can be tough to manage even for the most seasoned traders. That said, market sentiment and price-action have been rather orderly so far. Equity markets have been increasingly more volatile as seen in the latest bump-up in the VIX to the upper-20’s, but nowhere near the panic spike to 50 seen earlier in the year and in 2016.

Moreover, the percent of stocks in the S&P 500 below their 200-day Moving Average broke below -2 standard deviations from the mean and looks like it may need to test the -3 standard deviations threshold similar to moves in 2015 & 2016, before truly bottoming-out.

This, however, does not imply that more volatility is imminent, but merely a reference point to what may be needed to shift both sentiment and price-action back up.

Leave A Comment