Included with today’s second estimate GDP report by the Bureau of Economic Analysis is the preliminary estimate for third quarter corporate profits. The corporate profit measure is reported in several different formats, i.e. with and without inventory valuation and capital consumption adjustments. As I noted in a June post, more information on the adjustments can be found can be found in this BEA Briefing Paper (PDF).

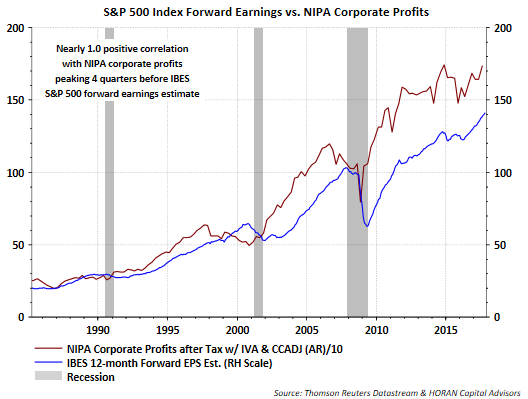

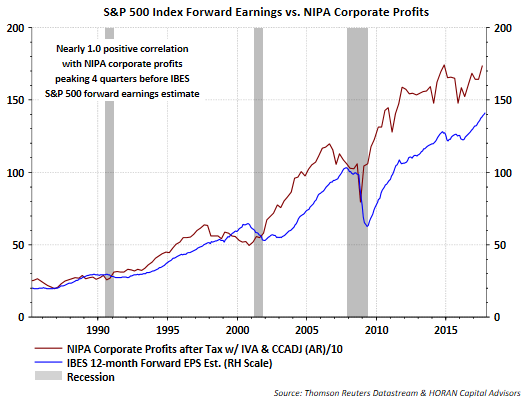

The profit growth before tax and with the inventory valuation and capital consumption adjustments equaled 5.4% on a year over year basis. Without the adjustments, year over year profit growth equaled 10%. Importantly, NIPA profits have a nearly 1.0 correlation to IBES S&P 500 forward earnings and historically peak four quarters, or a year before the IBES forward earnings estimate. This preliminary corporate profit report is not signaling a peak in IBES S&P 500 forward earnings.

Also, with the preliminary corporate profit growth figure, one can evaluate the NIPA P/E. The growth in NIPA corporate profits has resulted in a slight decline in the NIPA P/E as can be seen in the below chart. As I noted in the June post referenced above, what is useful with the NIPA profit measure is the fact it covers a larger earnings base for the U.S and covers more industries as it is not limited to public companies. Additionally, the NIPA figure makes an effort to adjust for the differing accounting measures being utilized by companies.

By reviewing some of my posts written over the past few months, the lack of any meaningful market pullback has been one recurring theme. However, with the continued strength exhibited in corporate profit growth, the market’s path is certainly warranted as stock prices follow earnings. Also, the strong profit picture is beginning to result in a downtrend in the market’s NIPA valuation, without a significant correction taking place. That does not mean high valuation equities will not correct more significantly, like what occurred in some technology stocks today. All in all, today’s revision higher in Q3 GDP and the preliminary profit report are both tailwinds for the economy and equity markets, all else being equal.

Leave A Comment