Courtesy of subdued gas price increases this year vs. one year ago, overall consumer prices rose only 0.1% in September vs. 0.5% one year ago (and 0.3% over the last two months vs. 0.9% one year ago). As a result, YoY CPI growth is down to 2.3% vs. 2.9% several months ago, and that means that “real” wages increased, despite no movement in growth nominally YoY.

With that background, let’s update real average and aggregate wages.

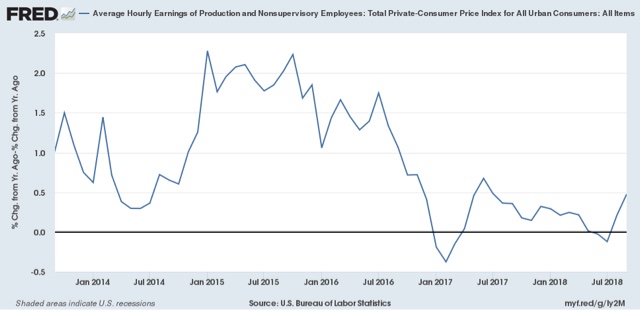

Since nominal wages for non-managerial workers are up 2.7% through September, this means that real wages, which had been flat, have grown in the last few months by +0.4% YoY:

In the last 2 1/2 years, real wages had been essentially flat. The last couple of months moves the needle a little bit:

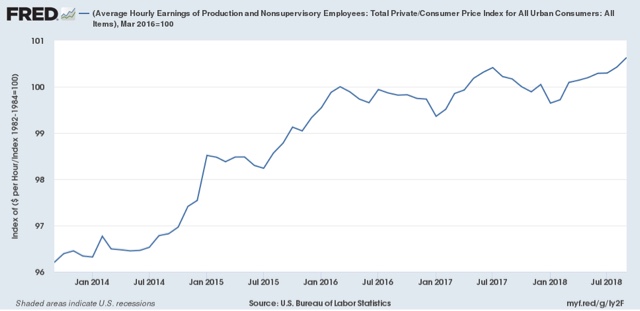

Further, because employment and hours have increased, real *aggregate* wage have continued to grow:

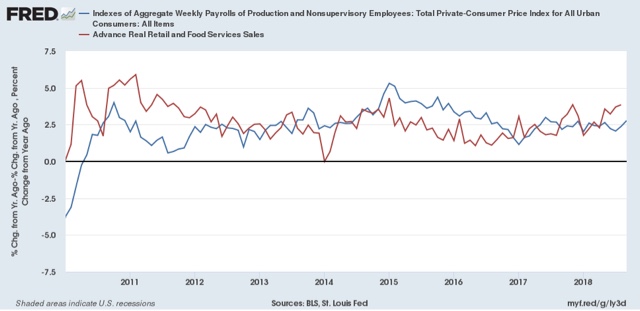

Real aggregate wages — the total earned by the American working and middle class — are now up 26.2% from their October 2009 bottom.

Finally, because consumer spending tends to slightly lead employment, let’s compare YoY growth in real retail sales, first measured quarterly (red), with that in real aggregate payrolls (blue):

Here’s the monthly close-up on the last 9 years:

Retail sales won’t be reported until next week. They grew +1.9% nominally last September, igniting some very good YoY comparisons that have been reflected in an acceleration of YoY employment growth as well. I am expecting a substantial downshift in retail sales next week, which in turn is likely to lead to a substantial downshift in employment reports beginning in a few months.

Related Posts

The Most Active Equity Options And Strikes For Midday – Thursday, Dec. 7

The Most Active Equity Options And Strikes For Midday – Thursday, Dec. 7 Why The Dow Jones Industrial Average Fell Today – November 23, 2015

Why The Dow Jones Industrial Average Fell Today – November 23, 2015 Weekly Unemployment Claims: Down Another 15K

Weekly Unemployment Claims: Down Another 15K- EUR/USD Rate Eyes August-High As Bearish Trends Start To Unravel

- Beyond Visa: 4 Great Financial Transaction Picks

Move Over ZIRP… Here Comes NIRP!

Move Over ZIRP… Here Comes NIRP!

Leave A Comment