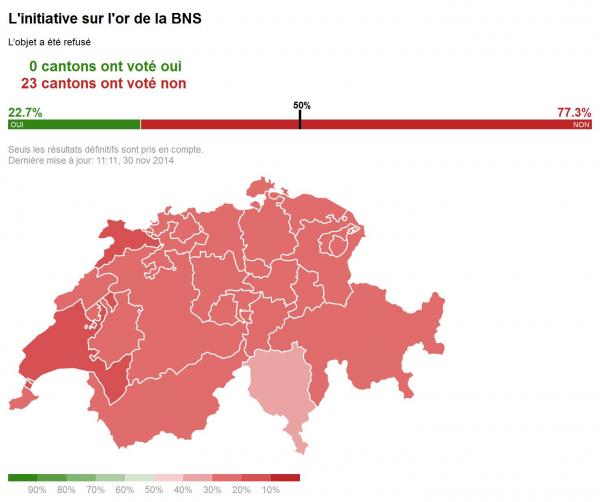

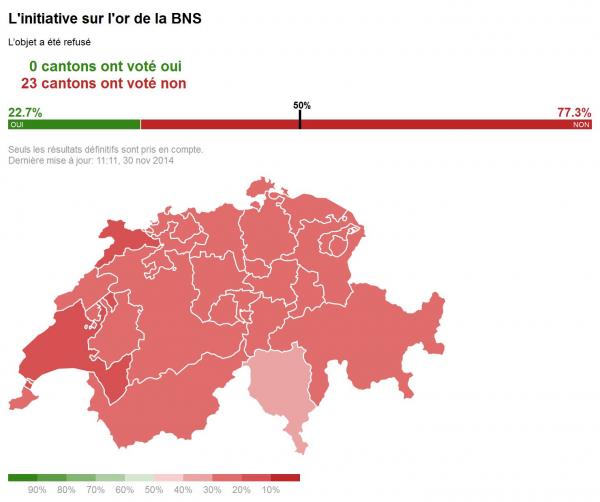

One year ago (and just two months before the shocking announcement the Swiss Franc’s peg to the Euro would end, dramatically revaluing the currency, and leading to massive FX losses around the globe and for the Swiss National Bank) the Swiss held a referendum whether to demand that their central bank should convert 20% of its reserves into gold, up from 7% currently. After the early polls showed the Yes vote taking a surprising lead, the Diebold machines kicked in and the result was a sweeping victory for the No vote, without a single canton voting for sound money.

Ironically, this unexpected nonchallance about the Swiss central bank’s balance sheet by one of Europe’s more responsible nations took place just before the same bank announced CHF30 billions in losses on its long EUR positionsfollowing the revaluation of the CHF. It also took place when not just Germany, but the Netherlands and Austria announced they would repatriate a major portion of their gold in a move which, all spin aside, signals rising concerns about the existing monetary system.

We wonder if the Swiss have changed their mind about just how prudent it is to have their central bank operate as one of the world’s largest – and worst – long EUR positions FX traders, and hedge funds with $94 billion in stock holdings, since then.

We may soon have the answer, because in what is shaping up to be another historic referendum on the treatment of money, earlier today the Swiss Federal Government confirmed that it had received enough signatures and would hold a referendum as part of the so-called “Vollgeld”, or Full Money Initiative, also known as the Campaign for Monetary Reform, which seeks to ban commercial banks from creating money, and which calls for the central bank to be given sole power to create the money in the financial system.

In other words, an initiative to ban fractional reserve banking, and revert to a 100% reserve.

Related Posts

3 Things: Everyone Gets A Trophy, Inflation & RCube

3 Things: Everyone Gets A Trophy, Inflation & RCube SEC to address growing crypto issuer filings with specialized offices

SEC to address growing crypto issuer filings with specialized offices- AUDUSD Daily Analysis – Monday, Dec. 18

- Is Pain Ahead For Healthcare ETFs After Weak JNJ Q1?

- Accommodative Officials And Synchronized Upturn Drive Markets

- Week In Review: WuXi AppTec Raises $1.5 Billion For China Healthcare

Leave A Comment