President Trump believes in bilateral trade negotiations, with tariffs, if necessary, to cure alleged imbalances. House speak Paul Ryan is on board with a Border Adjustment Tax (BAT) proposal.

Wall Street Journal writer Greg Ip says Deficits Are a Flawed Guide to Unfair Trade.

At least one of the positions is wrong.

President Donald Trump seems to be spoiling for a fight with some of America’s biggest trade partners. The problem is how he judges victory. “I’m trying to find a country where we actually have a surplus of trade as opposed to a deficit,” Mr. Trump groused last month.

The U.S. has a trade deficit because it consumes more than it produces. Lacking sufficient savings, the U.S. sells assets such as stocks, bonds or other IOUs to foreigners to finance consumption and capital spending. A trade deficit always equals an inflow of foreign capital.

This deficit arithmetic isn’t controversial; the dispute is over what causes it. Mr. Trump and Peter Navarro, director of his National Trade Council, blame unfair trade, arguing that other countries are cheating in the global trade arena. His critics say it’s the appeal of the U.S. as a destination for investment.

Both arguments are an oversimplification. Trade deficits and capital inflows result from a combination of U.S. and foreign saving, consumption, and investment behavior, much of it benign but some of it not.

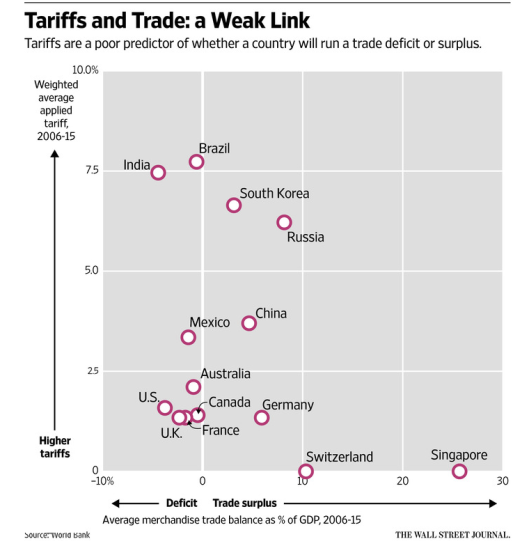

Mr. Trump’s argument implies there should be some correlation between protectionist barriers and the trade balance. There isn’t. Brazil and India are highly protectionist yet run persistent trade deficits because they save less than they invest. Conversely, Germany, and Switzerland have low tariffs yet run persistent trade surpluses because of their high saving relative to investment.

In the past, Chinese currency intervention and tight controls on capital inflows kept the yuan artificially cheap and its trade surpluses inflated. Brad Setser of the Council on Foreign Relations says Taiwan and South Korea have held down their currencies via currency intervention and by encouraging domestic investors to buy foreign assets and discouraging foreign investors from buying domestic assets.

These actions are legitimate cause for complaint. Yet finding an effective deterrent has eluded previous presidents and it’s not clear what Mr. Trump can do differently. Punishing China for manipulating its currency makes less sense now that China is trying to prop it up, rather than push it down as in the past.

Mr. Trump might use deficits to pick the wrong fights. Mexico runs a trade surplus with the U.S. Mr. Trump seems determined to fix it by renegotiating the terms of the North American Free Trade Agreement and slapping tariffs on companies that outsource production to Mexico.

But Mexico runs a trade deficit with the world as a whole. The U.S. would be attacking a country that on net is reducing the world’s excess of saving, not contributing to it. If the economic and diplomatic damage weren’t enough, that’s one more reason for the president to be careful about how he picks his battles.

Related Posts

SPX Bullish Scenario To 2510-20 Winning Points So Far

SPX Bullish Scenario To 2510-20 Winning Points So Far US gov’t debt downgraded — Huge news for Bitcoin?

US gov’t debt downgraded — Huge news for Bitcoin? Quant Crash: Human-Robot Blame Game Escalates As CTA, Risk Parity Scapegoating Reaches Fever Pitch

Quant Crash: Human-Robot Blame Game Escalates As CTA, Risk Parity Scapegoating Reaches Fever Pitch A Warning Shot For Passive Investing

A Warning Shot For Passive Investing What are the benefits of investing in smaller companies?

What are the benefits of investing in smaller companies? European High Yield Faces Two-Headed Hydra From Italy, EM FX

European High Yield Faces Two-Headed Hydra From Italy, EM FX

Leave A Comment