It’s conceptual possible, if not always practically convenient, to separate tax policy into two mainpieces. One issue is the tax cut vs. tax hike debate–that is, whether the total amount being collected should be higher or lower. The other issue is whether the tax code should be adjusted in some way to alter its incentives and disincentives. As one example, the 1986 Tax Reform Act was more-or-less neutral in the amount of revenue it collected, but it altered the incentives of the tax code by combining lower marginal tax rates with a reduction in the availability of various deductions, credits, and exemptions.

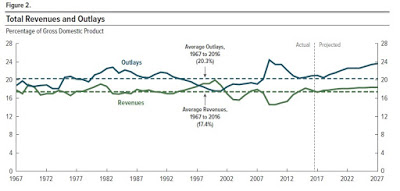

In thinking about the current tax bill, first consider the question of how US tax and spending compares with to historical levels. Here’s a figure from the Congressional Budget Office report, “An Update to the Budget and Economic Outlook: 2017 to 2027” (June 2017). A little-remarked fact about the present state of the federal budget is that the level of federal spending is almost exactly at its 50-year average of 20.3%, while the level of total federal taxes is pretty much right on its historical federal average of 17.4%. Thus, the budget deficit at present is also very close to its long-run average of 2.9% of GDP.

When looking at a government’s debt burden over time, the most useful quick metric is the ratio of total accumulated debt/GDP. Here’s a CBO figure from March 2017 showing this metric for the US economy over time–and projections for the next couple of decades. The common pattern over time is that the debt/GDP ratio rises sharply during wartime, and around times of extreme economic stress like the Great Depression of the 1930s and the more recent Great Recession.

But the Great Recession ended back in June 2009, and the US unemployment rate has been 5% or lower for more than two years, since September 2015. Moreover, the long-term projections from CBO suggest that existing government programs are going to exert very large pressures for higher government debt in the next couple of decades, as the boomer generation retires and health care costs continue to rise. When (and not if) the next recession arrives, it will be a good time to run larger deficits again. But the case for a tax cut to stimulate the US economy that reported a 4.1% unemployment rate in October 2017 is weak.

What about the effects of the tax bill on economic incentives?I sometimes use the analogy that economies carryinga tax burden are similar to a hiker carrying gear for a back-country excursion. If the hiker has a well-fitted and well-padded backpack, with the weight nicely distributed, it’s a lot easier to hike all day. If you took the exact same camping gear and randomly attached it to hiker around their body–some on the feet, the heaviest weight on the right arm and nothing on the left arm–that same amount of weight becomes very difficult to carry. Thus, the question of tax reform is not whether the burden should be higher or lower, but rather how best to distribute a given amount of weight.

There are of course lots of estimates of how the tax bill will affect incentives, but the estimates of the Joint Committee on Taxation are especially worthy of notice. Because Republicans control Congress, that party also controls the Joint Committee on Taxation. However, many staff members of the JCT soldier on from one administration to the next, showing both some willingness to be flexible as their political guidance changes, but also showing some stubbornness in insisting on a certain level of consistency and logic in their estimates. Thus, economists who tend to align with the Democratic party like Larry Summers, Jason Furman, and Paul Krugman have all been willing to cite the JCT estimates as a reasonable basis for discussion (although I’m sure they also disagree with these estimates in various ways).

Here are some comments from the JCT report. “Macroeconomic Analysis of the“Tax Cut and Jobs Act” as Ordered Reported by the Senate Committee on Finance on November 16, 2017” (November 30, 2017):

Leave A Comment