While one wouldn’t see it by looking at the S&P 500 which in fits and starts continues to push toward its January all-time highs, the latest weekly flows saw a broad “risk off” shift in investor mood, with $3.6BN out of equities ($0.7bn ETF outflows, $2.9bn mutual fund outflows), $2.3BN out of bonds, and $0.5BN out of gold.

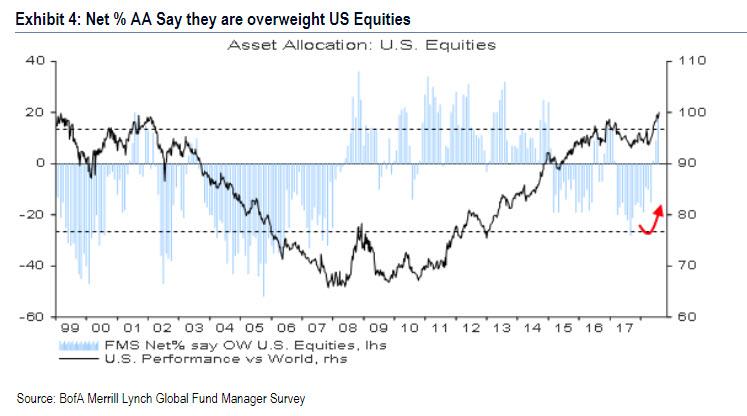

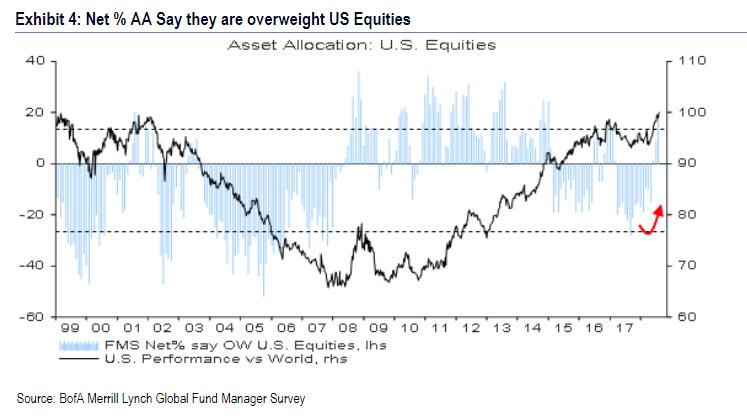

Curiously, despite the so-called decoupling between the US and the rest of the world, investors weren’t convinced, and pulled $2.6BN out of US equity funds, despite the recent BofA survey showing the biggest equity overweight by fund managers in US stocks since Jan ’15.

Meanwhile, it appears that at least according to fund flows, the leadership is finally broken. Remember this chart from a month ago, when BofA annualized tech inflows YTD and came up with a ridiculous number?

Well, the streak is now over and the last week saw the biggest Tech outflow since the Feb sell-off, as investors pulled$0.5bBN, together with big redemptions from Financials ($1.2bn).

Another streak that is clearly over in light of the recent EM fireworks, is that into Emerging markets, which also saw some $0.2BN in outflows. Meanwhile, Europe remains near rock bottom, with 23 consecutive weeks of outflows after the latest $2.9 billion in latest weekly outflows.

And as investors pulled money out of growth, the rushed into “late cycle” defensives, with big inflows to Healthcare ($0.8bn & $5.5bn inflows past 3 months = 4% AUM).

And speaking of late cycle, the top 5 performing S&P sectors in the past 3 month all defensive: staples, utilities, REITs, healthcare, telco.

Putting the above in context, here are the most overbought and oversold assets in August:

Leave A Comment