Well, here we are again.

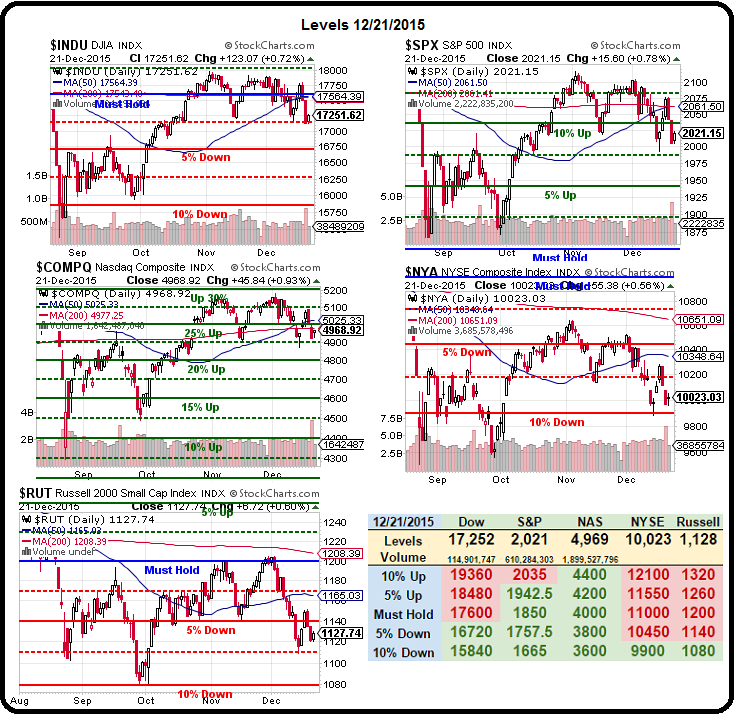

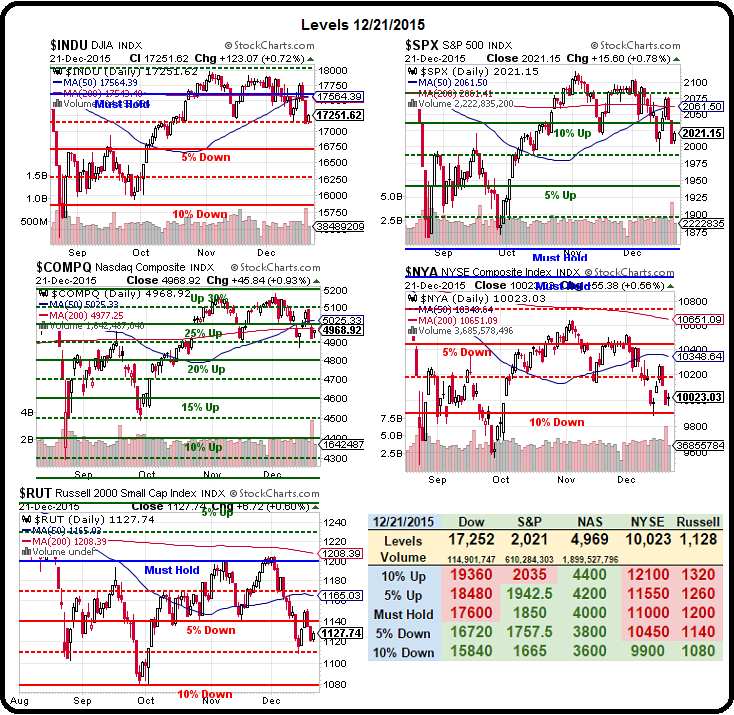

This is the third serious test of the 2,000 line on the S&P since October from the top and before that we failed it spectacularly in August and then it acted as a ceiling twice in September before being broken to the upside in a low-volume, BS rally based on false hopes that never actually panned out. And, speaking of things not panning out – we got our revised Q3 GDP, it’s very unlikely to save the markets.

You could see the TradeBots working overtime yesterday as the failed attempt to prop up the indexes in the Futures was successfully retried into the close and we finished almost where we began the day – up 0.8% low volume (Friday’s drop was on 3x the volume).

Neither Asia nor Europe were fooled by our fake enthusiasm and both continents are flattish for the day (7am). China’s numbers are so bad that the 2nd private company this quarter, Minxin,has suspended their PMI report as it too diverged from the Government’s “official” numbers by about 15% (lower, of course). They were suspended 6 hours before they were scheduled to be released this morning. Keep in mind November’s report was simply awful too:

The manufacturing PMI declined to 42.4 in November from 43.3 in October, while the non-manufacturing reading fell to 42.9 from 44.2, according the latest release. The factory gauge fell to a record low of 41.9 in August. China’s official PMI from the National Bureau of Statistics fell to a three-year low of 49.6 in November.

As Zero Hedge asked: ”

How could it be possible that official figures remain so ‘healthy’ when every private survey (pre-discontinuation) has shown utter collapse?

” We were shorting China’s ETF, FXI in November as they tested $40 again but we took the money and ran at $35, expecting China to do SOMETHING to boost their economy into the end of the year. So far, not much has happened and certainly nothing effective. If $34 doesn’t hold on FXI – look out below.

Leave A Comment