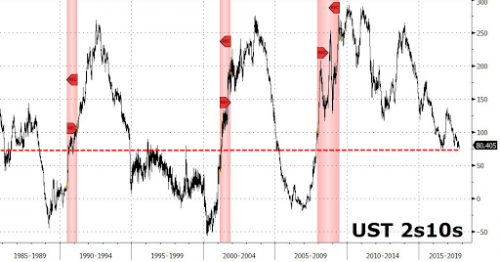

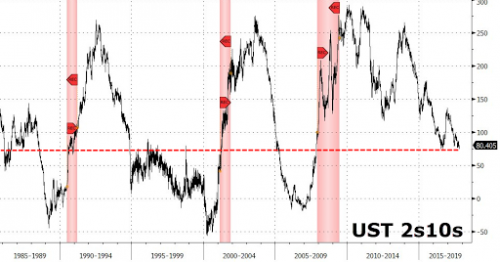

Last weekend, as Deutsche Bank’s derivatives strategist Aleksandar Kocic was looking at the spread between the short and long end of the curve, and while contemplating the lack of market volatility, he concluded that “given where long rates are, Fed appears as overly hawkish – it has only two more hikes to go and, for volatility and risk premia to reprice higher, the gap has to widen. As is appears unlikely that the Fed will be cutting rates any time soon, the gap could widen only if the Long rates sell off.”

In practical terms – if only for bond traders – this meant that “for anything to happen, 5Y5Y sector has to move higher”, however the $2.5 trillion question is whether this sell off in long rates will be violent or controlled. Kocic concluded that “This is the catalyst for everything.”

In other words, those lamenting the pervasive complacency and the ubiquitous lack of volatility in the market, may not have much more to wait: after just two more rate hikes, absent a parallel move wider across the rest of the curve, the Fed’s “breathing space” will collapse, and Yellen, or rather her successor, will lost control of both vol markets and long-dated yields, as the Fed effectively hikes into a self-made recession, where it itself inverts the yield curve. That would be a problem.

Incidentally, among Wall Street’s rates and derivatives strateigsts, the mixed – and polar opposite – signals being sent by the rates market has been all the rage in recent weeks, and everyone is eager to explain what happens next. For those who are unfamiliar, the conflicting dynamic sent by the bond curve is that “while the short end is optimistic, the long end has never been more pessimistic”, in the words of BofA’s rates strategist Shyam Rajan. And yet, in a paradoxical feedback loop, rarely has the near term meant more to the long term than today.

Here is how Rajan summarizes the “two-faced rates market”, in which the 2s10s is so flat it is a clear warning that all else equal, a recession is approaching:

Related Posts

Stocks Fall Despite Mostly Great Earnings

Stocks Fall Despite Mostly Great Earnings November Natural Gas Sinks Off The Board

November Natural Gas Sinks Off The Board E

Large Cap Best & Worst Report – March 22, 2016

E

Large Cap Best & Worst Report – March 22, 2016 The Truth About S&P 500 Earnings: No Growth For 7 Quarters, With A Revenue Recession On Top

The Truth About S&P 500 Earnings: No Growth For 7 Quarters, With A Revenue Recession On Top- Asian Shares Hit 10-Year Highs After Wall Street Record Close

What Does February Stock Market Crash Mean For Gold?

What Does February Stock Market Crash Mean For Gold?

Leave A Comment