Movies can have quite predictable plot lines that we know in advance – but we love them anyway. It could be a romance, where the girl is going to end up with the right guy through a series of improbable events, even though that looks impossible to begin with. It could be an action movie, where our tough and underestimated hero overcomes seemingly impossible odds to just barely win in the end, after all.

There are movies that play over and over again in the financial markets and the economy as well, and while the particulars change, the plots can repeat themselves.

In this analysis, we are going to take a look at a market “movie” that has played out twice in the modern era, and follow the A-B-C-D plot line that was followed in each case. We will then take a look at more recent events, see if A-B-C have been occurring, and ask if D could be coming after C for the third time in a row?

This analysis is part of a series of related analyses, an overview of the rest of the series is linked here.

The First Movie: The Tech Bubble & The Fed

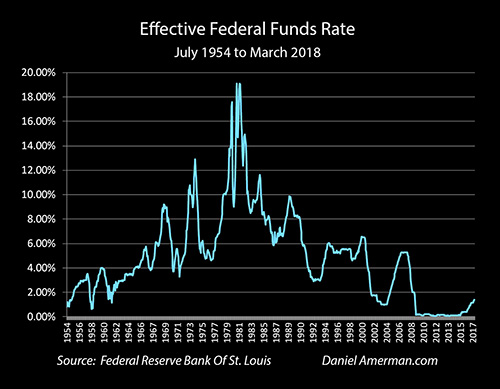

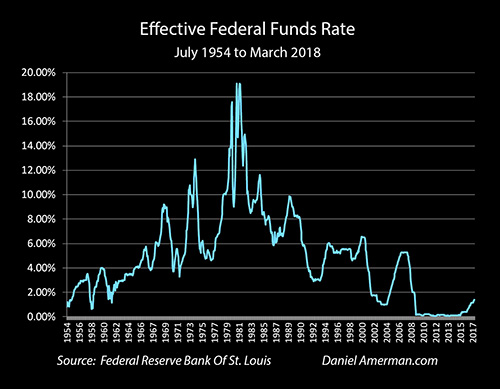

The above is a graph of the effective Federal Funds Rate from 1954 through March of 2018 (that final data point for March is not yet actual data, but is projected from the recent Fed meeting). Our starting point is the economic recession of 1990.

A. The Fed responded to the recession by using its primary economic weapon for rescuing a hurting economy – rapidly decreasing interest rates. The effective Federal Funds Rate was pushed down from 8.20% in September of 1990 to 2.92% in December of 1992.

As can be seen in the graph, that was the lowest interest rate in 30 years, interest rates had not been that low since they were at 2.90% in October of 1962.

B. The stimulus of lowering rates worked. The economy exited recession and began to grow again.

There was an acceleration a few years into the recovery. The economy was booming, and stock market prices began a rapid rise, particularly with the early tech stocks. A tech stock bubble was created, as many market pundits proclaimed a new era of unending prosperity, with far higher stock prices on the way.

C. The Fed initially responded to renewed economic growth by moving interest rates to a more historically normal range of around 5-6%, give or take.

However, by 1999, the Fed grew concerned that the economy was overheating, and that inflationary pressures could build. So the Fed deployed its primary tool for slowing down an overheating economy – increasing interest rates. The effective Federal Funds rate was pushed up from 4.76% in June of 1999 to 6.53% in June of 2000. That was an increase of about 1.75% in about a year.

D. The asset bubble collapsed, with crippling losses for investors. This collapse produced an immediate recession in 2001.

The recession of 2001 was not a normal business cycle recession. Yes, a falling stock market is associated with the recession, but this was something larger, a bubble popping, and the rapid and catastrophic collapse of wealth changed behavior, decisions and the economy.

This analysis is part of a series of related analyses, an overview of the rest of the series is linked here.

The Second Movie: The Real Estate Bubble & The Fed

A. The Fed responded to the recession by using its primary economic weapon for rescuing a hurting economy – rapidly decreasing interest rates. The effective Federal Funds Rate was pushed down from 6.40% in December of 2000 to 0.98% in December of 2003.

As can be seen in the graph, that was the lowest interest rate in almost 50 years, interest rates had not been that low since they were at 0.84% in November of 1954.

B. The stimulus of lowering rates worked. The economy exited recession, and began to grow rapidly.

In the process of pushing interest rates to the lowest levels seen in almost 50 years, the Fed also helped create the lowest mortgage rates most people had seen in their entire lifetimes. Low mortgage rates meant real estate prices could get much higher, without needing a higher income to qualify.

A real estate bubble was created. Many market pundits proclaimed a new era of unending prosperity, with a miracle formula for the creation of wealth by buying real estate.

C. By 2004, the Fed grew concerned that the economy was overheating. So the Fed deployed its primary tool for slowing down an overheating economy – increasing interest rates. The effective Federal Funds rate was pushed up from 1.00% in May of 2004 to 5.24% in July of 2006. That was an increase of about 4.25% in two years.

D. A sky-high real estate market ran into rapidly rising mortgage rates (along with a host of other issues), prices stopped climbing, and then they started falling. Numerous ill-considered risks in the financial markets also started to blow up, and the markets and the economy went into free fall.

There was another recession, sometimes called the Great Recession – and it was in no way a normal business cycle recession. It was created not by an overheated economy but by the popping of the real estate asset bubble and resulting cataclysmic damage to the financial markets.

Leave A Comment