Supercharged IPO is a new and controversial financial transaction that has dramatically increased in popularity over the past few years as companies try to extract as much value as possible from the IPO process.

A new white paper from Gladriel Shobe, Associate Professor, Brigham Young University Law School looks at the benefits of these transactions and considered whether the SEC should continue to allow such a process.

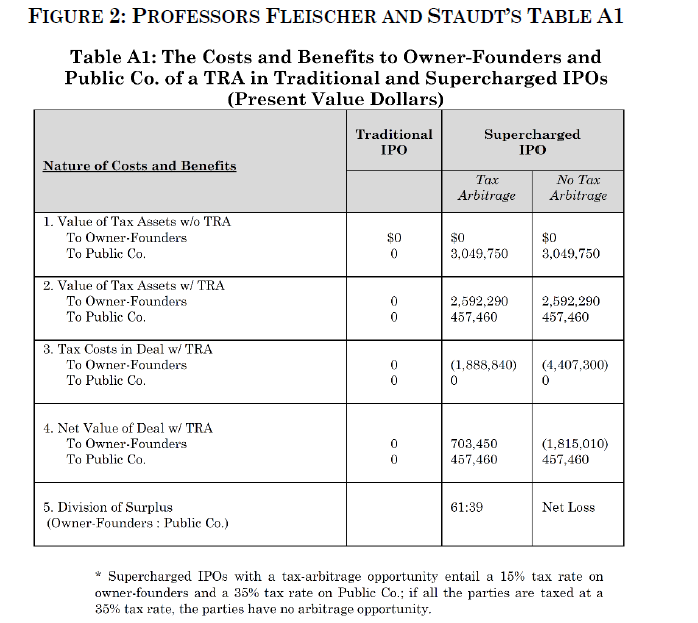

The supercharged IPO

The traditional IPO structure is comparatively inefficient from a tax perspective. That said, it can be “supercharged” to increases the basis of the assets of the newly public company thus increasing a number of depreciation deductions the new company can take against its future income. Using this method, the company can convert what is often its most valuable asset, its goodwill, from a non-depreciable asset to a depreciable one and the depreciation costs over the life of the asset will reduce the company’s future taxable income.

In a traditional IPO, to realize this supercharging, a change in structure is needed as, under the Internal Revenue Code, self-developed goodwill is not depreciable to the company that created the goodwill. If a different entity purchases the historic business, the tax code allows the purchaser to depreciate that same goodwill over a fifteen-year period. The Supercharged IPO goes one step further than the traditional method of supercharging a conventional IPO to add even more benefits. As the white paper explains:

“First, the owners structure the IPO as a sale so that the public company gets a step-up in the basis of its underlying assets, including self-developed goodwill. And second, the company and the pre-IPO owners usually enter into a contract called a “tax receivable agreement,” an agreement whereby the new public company makes payments to the pre-IPO owners for tax assets, including the tax assets created by the taxable sale.”

Leave A Comment