Recently, the US dollar has enjoyed a recovery, with some hawkish Fed speak for a change. However, the team at Credit Suisse still sees the downside:

Here is their view, courtesy of eFXnews:

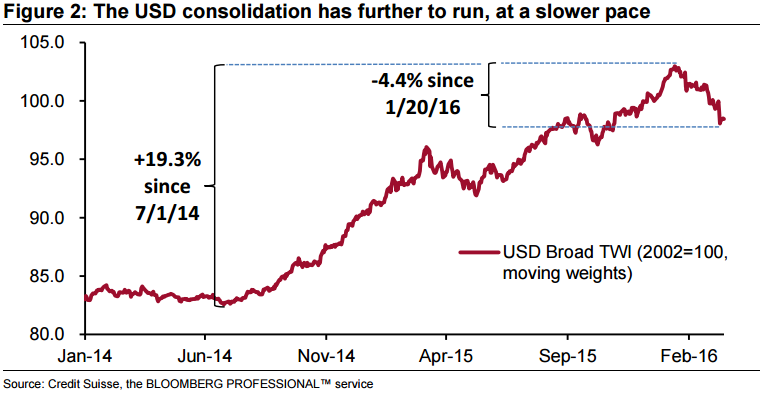

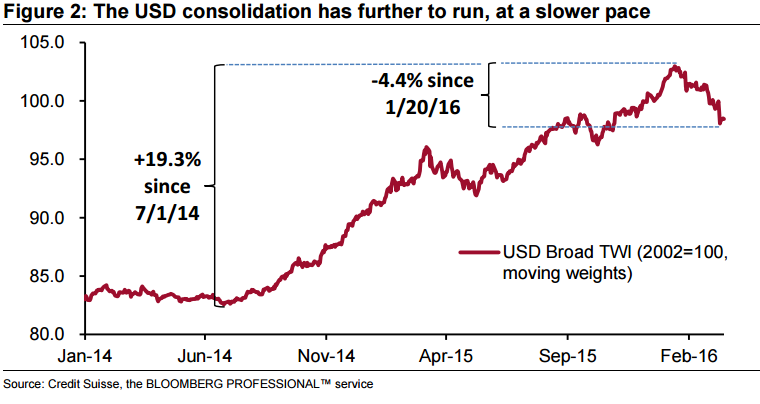

The sequence of volatile market reactions to central bank policy easing initiated by the BOJ and furthered by ECB had an eventful third round last week, as the Fed’s unexpected dovish shift caused a sharp retrenchment in long USD positions. As a result, the broad nominal USD has weakened further, extending its decline from the 20 January peak. We believe this trend has further scope to run in the near-term, and remain tactically bearish on the USD overall.

In contrast with the past few months, however, we think that implied volatility might be due for a pullback. The coming weeks are rather light on key central bank decisions, and that with the exception of the 7 April public appearance of Fed Chair Yellen, the occasions for significant challenges to the recently established central bank stances are few and far between over the course of the next month.

Looking towards Q2, we believe Brexit fears and central bank policy response to FX strength in commodity exporting countries could represent key challenges to the near-term bearish USD outlook. On the former front, we note that the pricing in of tail risks from Brexit appears well entrenched in GBP vol space, but much less so in other currencies. On the latter, we think a dovish policy reaction to further FX strength is more likely in Australia and New Zealand than in Canada.

Overall we remain long-term USD bulls.

Related Posts

Some Classic Short-Sale Candidates Get Even Better

Some Classic Short-Sale Candidates Get Even Better Market Talk – Tuesday, April 3

Market Talk – Tuesday, April 3 This service is declaring that it’s “crypto altseason” again

This service is declaring that it’s “crypto altseason” again “Bad Options” Regarding 2% Inflation Targets (And Other Silly Notions)

“Bad Options” Regarding 2% Inflation Targets (And Other Silly Notions) Some Important Stats On The Un-correlated History Of U.S. GDP And Stock Prices…

Some Important Stats On The Un-correlated History Of U.S. GDP And Stock Prices… DeSo offers $1M bounty for building decentralized Reddit

DeSo offers $1M bounty for building decentralized Reddit

Leave A Comment