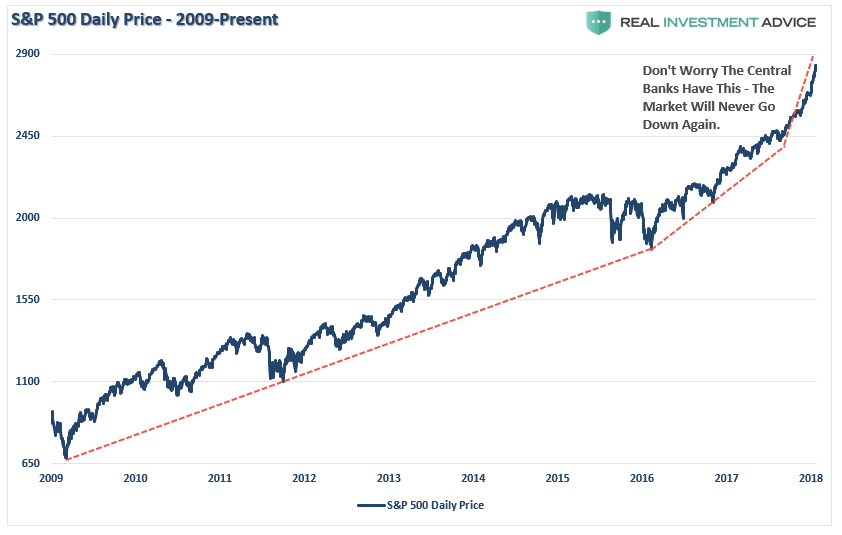

Since the beginning of the year, the acceleration in the markets has continued unabated. As I showed yesterday, the acceleration in the S&P 500 has now gone parabolic.

Of course, market melt-ups are symbolic of the final phases of “capitulation” as investors who feel like they “missed the boat,” finally jump back on board.

Such can be confirmed by the numerous emails from individuals asking me is “now the time to get back in?”

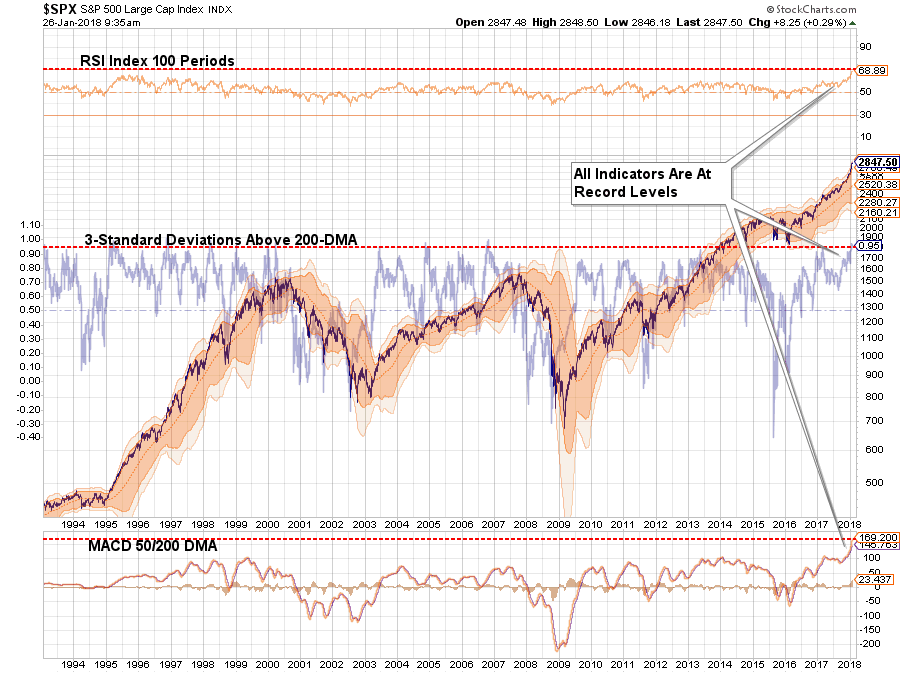

As shown in the chart below, such is the epitome of the “buy high, sell low” syndrome. Never before in recent history has the market been this overbought and extended from longer-term averages which suggests that a correction that reduces such conditions is highly likely in the near-term.

This doesn’t necessarily mean a “full blown” market crash, but even a correction back to the 200-dma, which is certainly within the scope of normal corrective actions, would currently entail a drawdown of almost -13%.

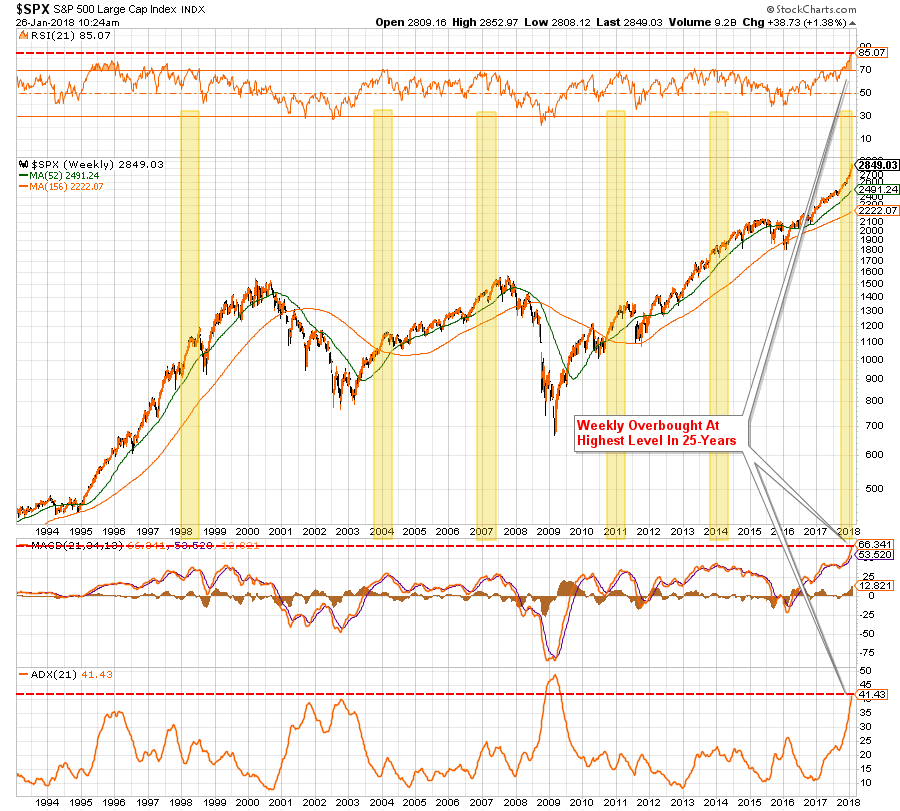

But let’s step back to a weekly chart and look at previous periods where historically high overbought conditions have existed previously.

On a weekly basis, a correction back to the 52-week moving average would require a bit more than a -14% decline while a correction back to the long-term trending average would be roughly -28%from current levels.

As I have said before, given we are now in the longest stretch in market history without even a 3% correction, 13% to 14% is going to “feel” worse than it is, and 28% will be equivalent to a full-fledged crash.

But just to keep that in perspective, a 28% decline from current levels only sets investors back to 2015. But, given that most investors are driven largely by emotion, those that have jumped in just recently, will be looking to “bail out” with that kind of a drop.

Buy high. Sell low.

Wash. Rinse. Repeat.

However, there’s nothing to worry about currently as long as the markets keep ratcheting up to new highs. As I penned last week in “The Honey Badger Market,”

“For now, it is hoped that historically high levels of stock valuations will be reduced by an explosion in underlying earnings growth due to the impact of tax reform.

While exuberance is currently ‘off the charts’ bullish, and our portfolios remain inherently long in the meantime, we are extremely cognizant of the risk of something ‘breaking.’

It is what always happens.

Yes, currently, everything is absolutely, positively, optimistic. Economic growth has picked up over the last couple of quarters due to an unprecedented level of natural disasters, oil prices have risen boosting production and corporate earnings, and employment is at historically high levels if you don’t count those out of the labor force.

The positive backdrop for stocks could not be currently better.”

Such is certainly the case for now.

The Davos Warnings

Meanwhile, in Davos, the confab of billionaires, world leaders, and the media have gathered for the annual confab in which the fate of the world is determined.

We were fortunate enough to obtain a clip from one of the speeches.

However, not all the views from Davos were of global tranquility and peace.

Barclays CEO Jes Staley, warned that financial markets remind him somewhat of what was seen before the 2008 crash.

“This feels a little bit like 2006. There are lots of reasons to be optimistic.

Global economic growth across the board is doing great at roughly 4%, unemployment rates in the U.K. and the U.S. are at almost record lows. All that is great. But all that comes amid ‘incredibly accommodating’ monetary policy, with interest rates that almost assume we’re still in recession.

If interest rates move too quickly and volatility whips around, things could get ‘interesting’ for markets over the next two years. It’s ‘concerning’ that people are selling short volatility even as it’s historically low, asset values are at all-time highs, and every major industry around the world last year grew by more than 20%.”

Axel Weber, chairman of the board of UBS AG, the Swiss bank, warned:

“Complacency in the markets is a key risk: Valuations are at unprecedented levels. The probability that we’ll encounter an unforeseen crisis on the next part of our journey is high.”

Related Posts

Stock Market Crash: 3 Things To Know In Case There’s A Sell-Off Ahead

Stock Market Crash: 3 Things To Know In Case There’s A Sell-Off Ahead Eurozone Commentary- Friday, October 27

Eurozone Commentary- Friday, October 27 SushiSwap CEO reveals DEX lost $30M on LP incentives this year

SushiSwap CEO reveals DEX lost $30M on LP incentives this year- GDP Forecasts Sink After Outstanding Jobs Report: GDPNow Vs Nowcast

- Daniele Sestagalli discusses Wonderland’s future after QuadrigaCX co-founder dox

Bull Of The Day: America’s Car-Mart

Bull Of The Day: America’s Car-Mart

Leave A Comment