Once a month, I assemble an economic forecast based on analysis of various data points which have led the economy. Historically, most of the time the economy trends up or trends down – but recently the economy simply has been frozen with little change in the rate of growth.

My view of the economy is at Main Street level – not necessarily GDP. My position is that GDP has disconnected from the real economy. A thinking person might say that GDP never projected the real economy – and it was never more obvious with the current situation where rate of change of growth slowed to a crawl. The jumping around of GDP in a flat economy is noticeable.

We will be releasing our economic forecast next week – and conditions have been flat (near the zero growth line) for three months. All indicators I view outside the elements of our forecast are mixed and confused. Nothing is strong.

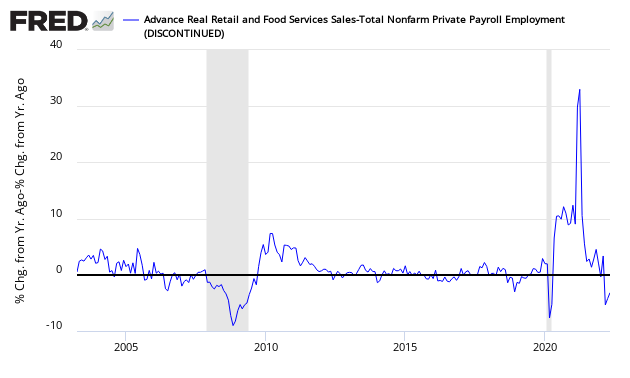

One of my favorite indicators to understand if the rate of economic growth is accelerating or decelerating is the relationship between the year-over-year growth rate of non-farm private employment and the year-over-year real growth rate of retail sales. This index is currently showing no growth differential. When retail sales grow faster than the rate of employment gains (above zero on the below graph) – the rate of growth of the economy is usually accelerating.

Growth Relationship Between Retail Sales and Non-Farm Private Employment – Above zero suggests economic expansion

One observation this week is the continuing improvement in the regional Fed’s manufacturing surveys where 3 of 4 regions are now showing manufacturing expansion. Manufacturing accounts for approximately 20% of the USA economy. I am not a fan of surveys, but when their indices jump into simultaneously – it makes you wonder.

Comparing Surveys to Hard Data:

At the same time, Markit PMI headlines US manufacturing PMI rounds off worst quarter since mid-2012:

Confused? My position is that manufacturing likely has reached the bottom of its long decline in its rate of growth – but that does not necessarily translate into a rapidly improving manufacturing situation.

Related Posts

Seagate Technology Shares Down Despite Strong Third-Quarter Earnings

Seagate Technology Shares Down Despite Strong Third-Quarter Earnings BoJ’s Patience Running Thin – USD/JPY To Prove Testy Around ¥110.00

BoJ’s Patience Running Thin – USD/JPY To Prove Testy Around ¥110.00 GBP/USD Bearish Trend Loses Momentum Near 1.35 And NFP

GBP/USD Bearish Trend Loses Momentum Near 1.35 And NFP Lam Research Corporation’s Q3 Earnings And Guidance Easily Top Expectations

Lam Research Corporation’s Q3 Earnings And Guidance Easily Top Expectations WTI Crude Oil And Natural Gas Forecast – Wednesday, March 8

WTI Crude Oil And Natural Gas Forecast – Wednesday, March 8- Fed Should Stick To A Schedule To Raise Rates

Leave A Comment