Mean reversion is “a concept of normality,” where extreme events can cause an asset to diverge from its long-term averages. For Deutsche Bank Foreign Exchange Macro Strategist Sebastien Galy, the theory of mean reversion works, so long as the underlying economic principles that exert the law of gravity on currency prices don’t change. Looking at currency markets, however, Galy notes that sometimes currency valuations and prices just don’t revert to their mean. This can be particularly when prudent government policies are not maintained.

Currency valuations follow a formula

Currencies have traditionally been valued based on a formula, of sorts, with a variance being afforded to developed world nations over emerging market countries to various degrees. When Argentina lifted its peg to the US dollar and allowed the currency to free float, it was not luck that led former JPMorgan banker turned Argentine Finance Minister Alfonso Prat-Gay to predict the estimated value of the currency. The same was the case when the Swiss left the euro currency, as the value was immediately calculated by the market in a flash.

In many cases, central bank involvement in interest rates plays a key role in currency value, and this can be particularly noticeable in emerging markets. Central banks intervene in their currency to lower make exports more competitive, which is accomplished in part by lowering interest rates but also through market supply and demand adjustments.

“A country intervenes in its currency primarily as a form of insurance for its export sector,” Galy noted in an August 22 report titled “The fear of asset bubbles.”

“The result is an amplification of currency intervention much as an orchestra tumults to the aria,” he wrote. “As this mechanism eventually fades lower so will the official demand for US Treasuries.”

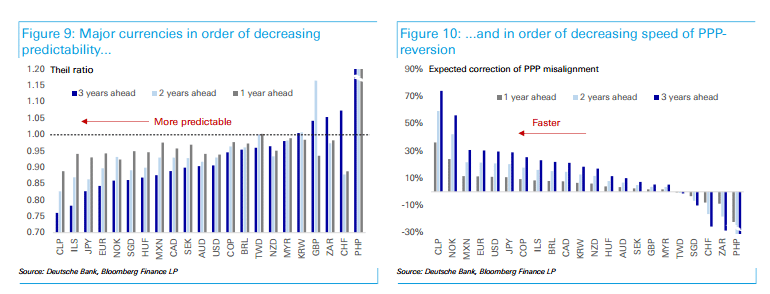

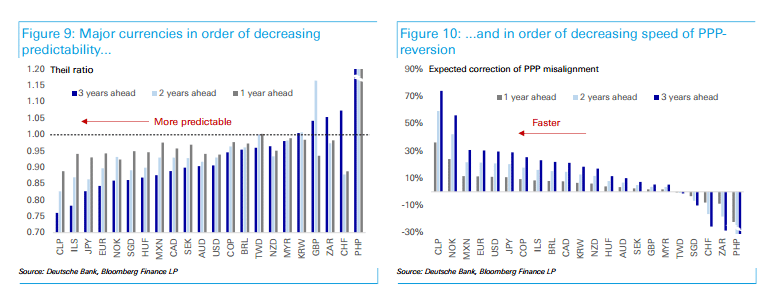

Currency valuations- mean revert, so long as core economic fundamentals remain intact

Leave A Comment