Fundamental Forecast for USDOLLAR: Bearish

– December rate hike practically a lock since the November NFP release.

– Recent economic data points to a “dovish liftoff’ – a reduced expected future rates path.

– Historical precedence around rate hike cycles beginning is messy at best.

This week is when the rubber meets the road after months – years, even – of qualified remarks, convoluted press conferences, and opaque policy statements: the Federal Reserve will finallyget on with it and raise its benchmark interest for the first time in nearly a decade. Historically, the Fed finds itself raising rates at a time when the labor market/inflation dynamic is just supportive enough to allow for policy tightening. Yet conditions today are relatively weaker than when the Fed raised rates last in June 2006:

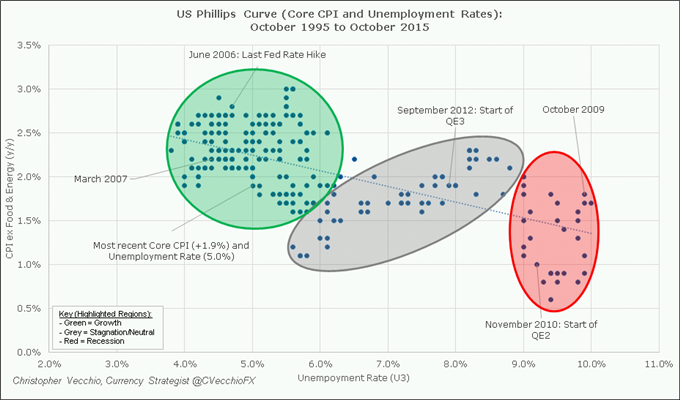

Chart 1: The US Phillips Curve: October 1995 to October 2015

When the Fed raised rates last in June 2006, the Unemployment Rate was 4.6% and Core CPI was +2.6% y/y. The most recent Core CPI (+1.9% y/y) and Unemployment Rate (5.0%) readings suggest that this is a softer environment to hike rates in that in past cycles. The recognition of this reality is the cornerstone of our belief that, despite the US Dollar having been supported by higher US yields and thus rising rate expectations in 2015, the path is anything but clear going forward after the Fed’s meeting on December 16.

Much like the European Central Bank’s decision to cut its deposit rate on December which subsequently produced a Euro rally, it’s more than likely that the upcoming Fed rate hike has been priced into the US Dollar, leaving open the possibility of disappointment. In fact, the process of the rate hike being priced into markets has been the backbone of the US Dollar rally over the past three months:

Chart 2: USDOLLAR Index vs December 2015 and June 2016 Rate Hike Probabilities

Related Posts

Between Order And Chaos In The S&P 500

Between Order And Chaos In The S&P 500 Learning From History And Modeling: Chinese Trade Retaliation Choices

Learning From History And Modeling: Chinese Trade Retaliation Choices A Look At The EIA Report And Some General Market Commentary

A Look At The EIA Report And Some General Market Commentary BofA: “The Market Implies There Is No Way A Shock Can Happen”

BofA: “The Market Implies There Is No Way A Shock Can Happen” Forex Forecast And Cryptocurrencies Forecast For August 20 – 24, 2018

Forex Forecast And Cryptocurrencies Forecast For August 20 – 24, 2018- US Dollar Bottoming Effort Takes A Step Forward

Leave A Comment