It’s long been an article of faith in the sound money community that the Fed, by bailing out every dysfunctional financial entity in sight, would eventually be forced to choose between the deflationary collapse of a mountain of bad debt and the inflationary chaos of a plunging currency.

That generation-defining crossroad is finally in sight.

On one hand, a tight labor market is pushing inflation to levels that normally call for higher interest rates:

source: tradingeconomics.com

source: tradingeconomics.com

Today’s Fed-heads are old enough to remember the 1970s when failure to get inflation under control produced a decade-long monetary crisis that was only resolved with (not exaggerating here) interest rates approaching 20%.

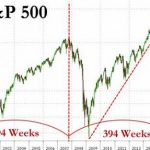

On the other hand, the yield curve – the difference between long-term and short-term interest rates – is trending towards zero and will, if it keeps falling, invert, meaning that short rates will exceed long. When this has happened in the past a recession has ensued.

With a system this highly leveraged it’s completely possible that the next recession will threaten the whole fiat currency/globalization/fractional reserve banking world. No one at the Fed wants to preside over that, leading some to view rising inflation as the lesser of two evils. See Atlanta Fed Chief Pledges to Oppose Hike Inverting Yield Curve.

A lot of people seem to be aware of the Fed’s dilemma. Here’s an excerpt from a recent Reuters article on the subject:

Fed’s Powell between a rock and hard place: Ignore the yield curve or tight job market?

Unemployment near a 20-year low screams at the U.S. Federal Reserve to raise interest rates or risk a too-hot economy. The bond market, not far from a state that typically precedes a recession, says not so fast.

The decision of which to heed looms large when the Fed’s interest-rate setters meet next week. Which path they follow will begin to define whether Chairman Jerome Powell engineers a sustained, recession-free era of full employment, or spoils the party with interest rate increases that prove too much for the economy to swallow.

New Fed staff research and Powell’s own remarks seem to put more weight on the risks of super-tight labor markets, which could mean a shift up in the Fed’s rate outlook and a tougher tone in its rhetoric.

Goldman Sachs economists, for instance, contend the Fed’s “optimal” rate path is “well above market pricing under a broad range of assumptions.” They see four increases likely next year, while investors expect only one or two, a significant gap.

Leave A Comment