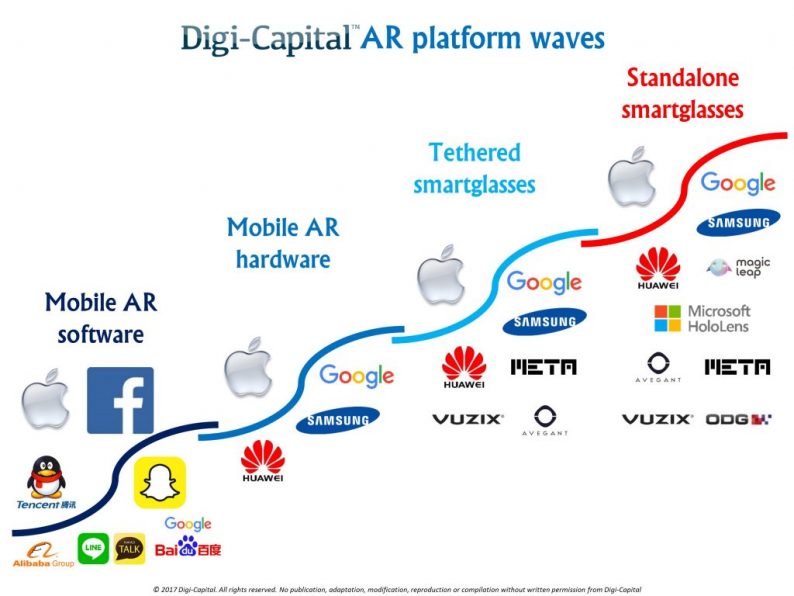

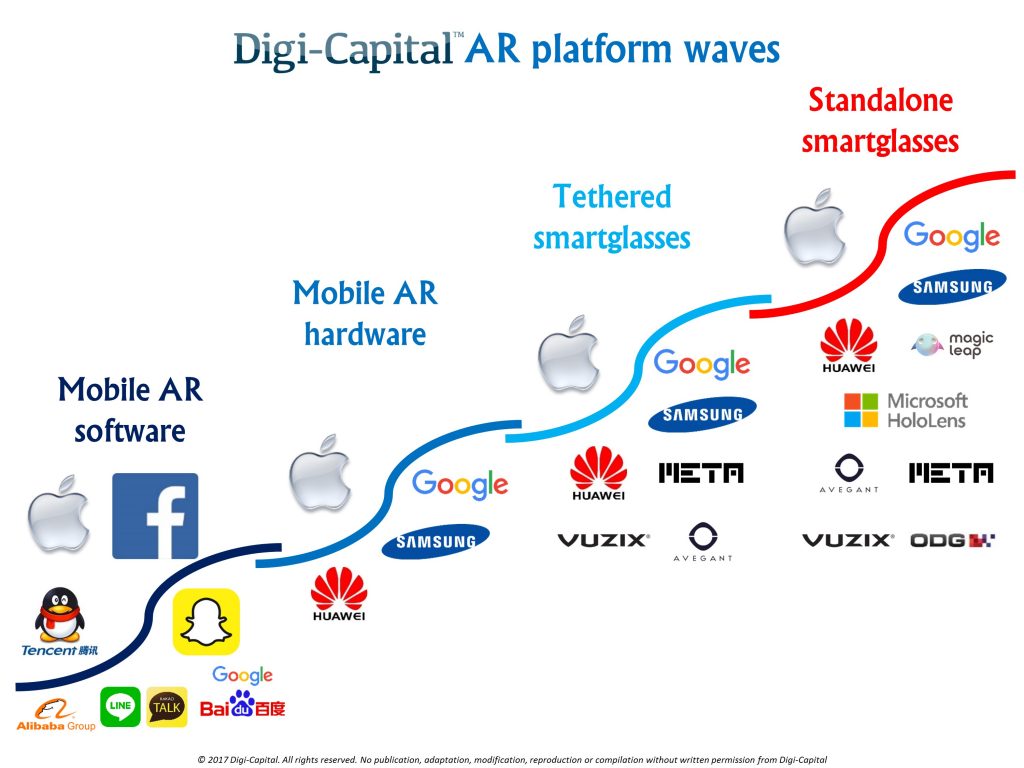

We’ve been saying for the last couple of years that Augmented/Virtual Reality is the fourth wave of consumer technology, and that AR could become much bigger than VR. But AR itself is not one giant wave, it’s a set of four big ones: mobile AR software, mobile AR hardware, tethered smartglasses and standalone smartglasses. These four waves could drive AR from tens of millions of users and $1.2 billion last year, to over a billion users and $83 billion by 2021. Surf’s up.

Consumer technology waves are not all the same. Some are ripples, others start small and swell to great heights, and there’s an occasional tsunami. So what is each AR wave? Let’s start by defining them:

Mobile AR software

Mobile AR software is the tsunami that came out of nowhere, with Pokémon Go downloaded 750 million times in its first year. But where Pikachu gave consumers their first taste of mobile AR, Facebook’s AR Platform and Apple’s ARkit for iOS democratize mobile AR software at scale as true consumer platforms.

Apple’s ARkit for iOS requires at least an iPhone 6S, iPhone SE, 2017 iPad or iPad Pro, with 300 to 400 million ARkit compatible devices today. 86% of iOS users installed iOS 10 a year after launch, so assuming iOS 11 follows a similar path and iPhones/iPads keep selling, ARkit could have an installed base up to 400 million devices by the end of 2018.

Facebook’s Camera Effects Platform is being rolled out to Facebook Messenger’s 1.2 billion MAU, WhatsApp’s 1.2 billion MAU, and Instagram’s 700 million MAU (with significant overlap). Facebook migrated 15% of WhatsApp users to Status 10 weeks after launch, 29% of Instagram users to Stories less than a year after launch, and 54% of Instagram users to Direct 4 years after launch. A similar growth curve could deliver around 400 million installed base for Facebook’s Camera Effects Platform by the end of 2018 too.

As well as these two dominant platforms, mobile AR software is set to play out across messaging apps from Tencent, Snap, LINE, Kakao and Snow, maps apps from Google and Baidu, eCommerce apps from Alibaba, Amazon, and eBay, plus consumer (non-games), enterprise, games, location based, video and other new mobile AR apps nobody has thought of yet. The over a billion users by 2021.

As with early iOS/Android, a Cambrian explosion of mobile AR apps with new dominant forms should emerge on top of these platforms (see hundreds of examples already on Digi-Capital’s mobile AR YouTube channel here), making them a bonanza for developers. As mobile AR software players will be able to migrate to mobile AR hardware, tethered smartglasses and standalone smartglasses waves, mobile AR software looks like the one wave to rule them all.

Mobile AR hardware

Mobile AR hardware’s additional sensors, CPU/GPU grunt, and AR focused device efficiency could improve user experience where computer vision and simultaneous localization and mapping (SLAM) are critical. This is despite the fact that Apple’s ARkit for iOS and Facebook’s Camera Effects Platform apps will work just fine on many standard smartphones.

With phone replacement cycles at 2½ years and high-end phones anywhere between 1/3 and 2/3 of smartphone sales (depending on manufacturer and geography), range-topping AR phones could deliver an installed base of tens of millions in the next 12 months, and $83 billion by 2021. In other words, mobile AR hardware might take 5 years to reach the same scale as just one of the dominant mobile AR software platforms next year.

Related Posts

Trading Support And Resistance – July 9

Trading Support And Resistance – July 9 UK Inflation Misses – GBP/USD Loses Ground

UK Inflation Misses – GBP/USD Loses Ground How Overvalued Is The S&P 500?

How Overvalued Is The S&P 500?- The Problem With The Global ‘Dollar Short’ Is The ‘Short’ Far More Than The ‘Dollar’

Median Home Price And Salaries Required In 27 Major Cities

Median Home Price And Salaries Required In 27 Major Cities Shanghai Composite Down 30.12% Since January 26th

Shanghai Composite Down 30.12% Since January 26th

Leave A Comment