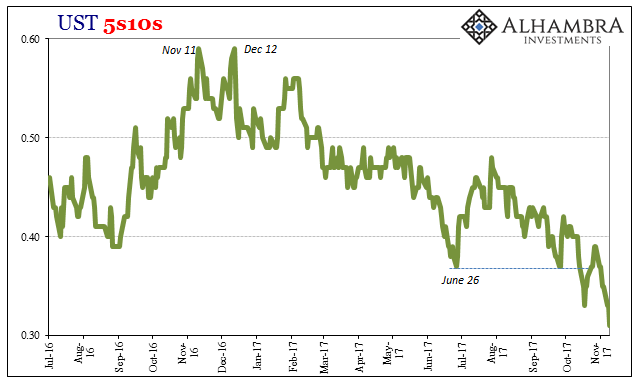

While I commend the mainstream media for refraining the past few months from their orthodox tendencies to shout BOND ROUT!!! every time long Treasury yields rise for more than a few days at a time, that doesn’t mean the total absence of the ridiculous. With the long end once again trending lower in nominal yields, the curve has utterly collapsed well past last summer’s low point(s), a condition that leaves most commentary stunned.

After all, the Fed undertaking “rate hikes” is supposed to signal their concerns about rising inflation and economic potential. Though neither of those is currently indicated anywhere, though they should have been a long time ago, the media continues to take Economists’ projections at face value. Editorial standards are as constant as the “conundrums” they have produced.

This has led to an overabundance of articles and stories all declaring how the bond market is surely wrong (without noting how right it has been for a very long time, directly in the face of Economists) and will live to really regret fighting the Fed. These are often created by logical fallacies (appeal to authority, in the form of either Bond Kings or Fed Kings), or, as in the case here, the preposterous.

What propelled the glut was demographic patterns in big economies that saw a surge in the share of people aged 35 to 64, which tend to be years of high savings, Will Denyer, an economist at Hong Kong-based Gavekal, wrote in a report this month. When those demographic patterns reverse, the implication will be potentially “big rate rises” and the risk of a “major fall” in global equity valuations, he wrote.

The “glut” discussed here is Ben Bernanke’s “global savings glut”, a figment he imagined a decade ago to explain why monetary growth outside the United States even in dollars just had to be someone else’s doing (and therefore responsibility). As I told my audience in the Cayman Islands last month, this idea was the only way that Economists like Bernanke could make sense of what was actually happening.

Related Posts

Indian Indices Trade Marginally Lower; Consumer Durables Stocks Witness Selling

Indian Indices Trade Marginally Lower; Consumer Durables Stocks Witness Selling CBN Boosts Forex Liquidity With Another $286m

CBN Boosts Forex Liquidity With Another $286m IBM Seems To Be Making Slow But Steady Progress

IBM Seems To Be Making Slow But Steady Progress Breakout In Nasdaq 100

Breakout In Nasdaq 100 Uncertainty prevails as December 2021 Bitcoin futures show an inverted pattern

Uncertainty prevails as December 2021 Bitcoin futures show an inverted pattern- Sensex Continues Downtrend; Metal Stocks Top Losers

Leave A Comment