During the 40 months after Alan Greenspan’s infamous “irrational exuberance” speech in December 1996, the Nasdaq 100 index rose from 830 to 4585 or by 450%. But the perma-bulls said not to worry: This time is different—-it’s a new age of technology miracles that will change the laws of finance forever.

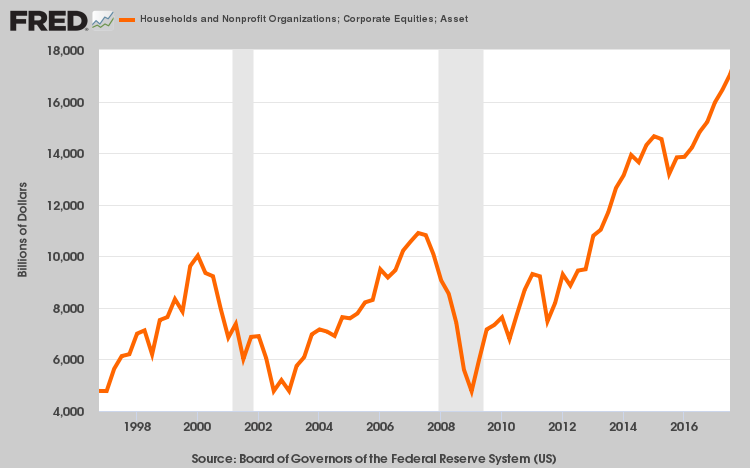

It wasn’t. The market cracked in April 2000 and did not stop plunging until the Nasdaq 100 index hit 815 in early October 2002. During those heart-stopping 30 months of free-fall, all the gains of the tech boom were wiped out in an 84% collapse of the index. Overall, the market value of household equities sank from $10.0 trillion to $4.8 trillion—-a wipeout from which millions of baby boom households have never recovered.

Likewise, the second Greenspan housing and credit boom generated a similar round trip of bubble inflation and collapse. During the 57 months after the October 2002 bottom, the Russell 2000 (RUT) climbed the proverbial wall-of-worry—-rising from 340 to 850 or by 2.5X.

And this time was also held to be different because, purportedly, the art of central banking had been perfected in what Bernanke was pleased to call the “Great Moderation”. Taking the cue, Wall Street dubbed it the Goldilocks Economy—-meaning a macroeconomic environment so stable, productive and balanced that it would never again be vulnerable to a recessionary contraction and the resulting plunge in corporate profits and stock prices.

Wrong again!

During the 20 months from the July 2007 peak to the March 2009 bottom, the RUT gave it all back. And we mean every bit of it—-as the index bottomed 60% lower at 340. This time the value of household equities plunged by $6 trillion, and still millions more baby-boomers were carried out of the casino on their shields never to return.

Now has come the greatest central bank fueled bubble ever. During nine years of radical monetary experimentation under ZIRP and QE, the value of equities owned by US households exploded still higher—-this time by $12.5 trillion. Yet this eruption, like the prior two, was not a reflection of main street growth and prosperity, but Wall Street speculation fostered by massive central bank liquidity and price-keeping operations.

Nevertheless, this time is, actually, very different. This time the central banks are out of dry powder and belatedly recognize that they have stranded themselves on or near the zero bound where they are saddled with massively bloated balance sheets.

So an epochal pivot has begun—-led by the Fed’s committement to shrink its balance sheet at a $600 billion annual rate beginning next October. This pivot to QT (quantitative tightening) is something new under the sun and was necessitated by the radical money printing spree of the past three decades.

What this momentous pivot really means, of course, is ill understood in the day-trading and robo-machine driven casinos at today’s nosebleed valuations. Yet what is coming down the pike is nothing less than a drastic, permanent downward reset of financial asset prices that will rattle the rafters in the casino.

This time is also very different because there will be no instant financial market reflation by the central banks. And that means, in turn, that there will be no fourth great bubble, either. Here’s why.

Related Posts

Bitcoin futures open interest at 2023 high while BTC trading volume at yearly low — What gives?

Bitcoin futures open interest at 2023 high while BTC trading volume at yearly low — What gives? Thai SEC wants to lift restrictions on initial coin offerings

Thai SEC wants to lift restrictions on initial coin offerings- Cointelegraph’s Top 10 in blockchain are here, but why should anyone care?

Amazon.com, Inc. Stock Downgraded By 1 Firm As Most Others Boost PT

Amazon.com, Inc. Stock Downgraded By 1 Firm As Most Others Boost PT Best Of The Nasdaq 100

Best Of The Nasdaq 100 Stocks Watch-List: WYNN, WHR, WDC

Stocks Watch-List: WYNN, WHR, WDC

Leave A Comment