The risk of owning cryptocurrency is pretty simple.

You could lose money… but that’s a risk that comes with ANY investment.

Every sane crypto investor understands this going in.

But what about the risks of NOT owning cryptocurrencies?

Those are very real too…

What if bitcoin ownership goes from less than 1% to 10%? How about 35%?

What if current debt-based monetary systems are doomed in the long term?

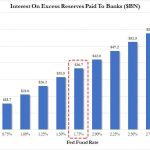

What if central banks lose their monopoly on legal tender? (It already happened in Japan.)

What if our savings continue to be debased by reckless monetary policy?

What if cryptocurrency prices only peak and stabilize after decades, when the majority of people are invested?

What if bitcoin owners shift some profits into other cryptocurrencies that have improved on the original idea?

What if we could choose from many different types of money?

What if we don’t need banks?

Finally, what if we’re in the early stages of a financial revolution?

These questions should reinforce the magnitude of what we’re talking about here.

If you don’t own any, you risk missing out on what could be the greatest wealth generation event ever.

Cryptocurrency a No-Brainer for Retirement Planning?

I believe cryptocurrency should be part of every investor’s retirement portfolio. It doesn’t have to start out as a big chunk of your holdings. But for the reasons I explained above, I believe the risks of not owning it are high.

Cryptocurrency is technologically superior to traditional monetary systems. It is independent, decentralized and has crazy momentum going for it.

We’re adding millions of new owners per month. This is exactly how the beginning of “going mainstream” would look.

Institutional interest is rising, and many firms are now dipping their toes in. Coinbase just announced a custodial service for hedge funds and other financial groups looking to diversify into cryptocurrencies. It thinks there could be $10 billion in institutional money on the sidelines. I suspect it’s higher than that.

Related Posts

US Futures Tread Water Ahead Of “Average Hourly Earnings” Report

US Futures Tread Water Ahead Of “Average Hourly Earnings” Report $21 Trillion And Counting: Fed Misdirection And Powell’s Powder Puff Presser (Part 4)

$21 Trillion And Counting: Fed Misdirection And Powell’s Powder Puff Presser (Part 4) Another Day, Another Intervening BoJ

Another Day, Another Intervening BoJ Bitcoin part of highest risk category in Basel’s new bank capital plan

Bitcoin part of highest risk category in Basel’s new bank capital plan- E

Oracle Vs. Google Case Goes To Jury

Rising Systemic Risk For All Markets

Rising Systemic Risk For All Markets

Leave A Comment