There will be an extremely painful oil supply shortfall sometime between 2018 and 2020. It will be highly disruptive to our over-leveraged global financial system, given how saddled it is with record debts and unfunded IOUs.

Due to a massive reduction in capital spending in the global oil business over 2014-2016 and continuing into 2017, the world will soon find less oil coming out of the ground beginning somewhere between 2018-2020.

Because oil is the lifeblood of today’s economy, if there’s less oil to go around, price shocks are inevitable. It’s very likely we’ll see prices climb back over $100 per barrel. Possibly well over.

The only way to avoid such a supply driven price-shock is if the world economy collapses first, dragging demand downwards.

Not exactly a great “solution” to hope for.

Pick Your Poison

This is why our view is that either

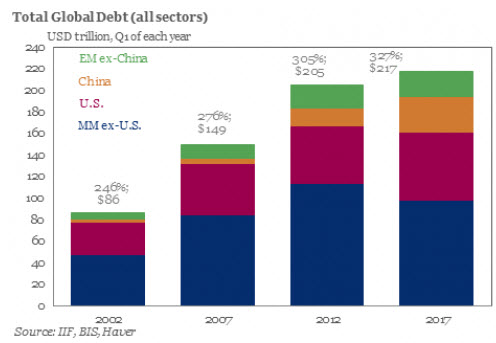

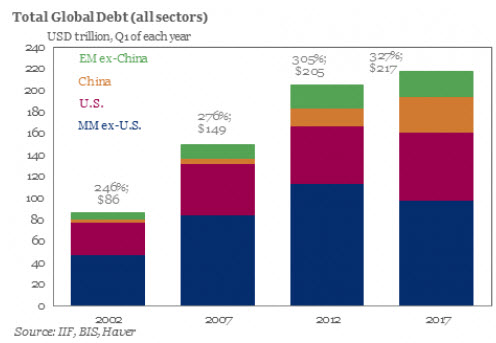

If (1) happens, the resulting oil price spike will kneecap a world economy already weighted down by the highest levels of debt ever recorded, currently totaling some 327% of GDP:

(Source)

Remember, in 2008, oil spiked to $147 a barrel. The rest is history — a massive credit crisis ensued. While there was a mountain of dodgy debt centered around subprime loans in the US, what brought Greece to its knees wasn’t US housing debt, but its own unsustainable pile of debt coupled to a 100% dependence on imported oil — which, figuratively and literally, broke the bank.

If (2) happens, then the price of oil declines, if not collapses. Demand withers away, the oil business cuts back on its exploration/extraction investments even further, so that much later, when the global economy is trying to recover, it then runs into an even more severe supply shortfall. It becomes extremely hard to get sustained GDP growth back online.

Related Posts

Professional Traders Position Management In Forex Trading – Hedging, Portfolio And Money Management

Professional Traders Position Management In Forex Trading – Hedging, Portfolio And Money Management Elizabeth Warren compares ‘bogus’ crypto to ‘legitimate’ CBDCs in senate hearing

Elizabeth Warren compares ‘bogus’ crypto to ‘legitimate’ CBDCs in senate hearing UK Services PMI Misses With 53.3 – GBP/USD Falls

UK Services PMI Misses With 53.3 – GBP/USD Falls- Energy Ideas For Contrarians

- The Greek Tragedy Is Far From Over

Macro Changes For Gold And Stocks

Macro Changes For Gold And Stocks

Leave A Comment