The long-term economic oscillations between boom and bust are caused by changes in the money-supply growth rate. It can therefore make sense to monitor such changes, but doing so requires knowing how to calculate the money supply. Unfortunately, most of the popular monetary aggregates are not useful in this regard because they either include quantities that aren’t money or omit quantities that are money.

What “Austrian” economists refer to as TMS (True Money Supply) is the most accurate monetary aggregate. Whereas popular measures such as M2, M3 and MZM contain credit instruments, TMS only contains money. Specifically, TMS comprises currency (notes and coins), checkable deposits and savings deposits.

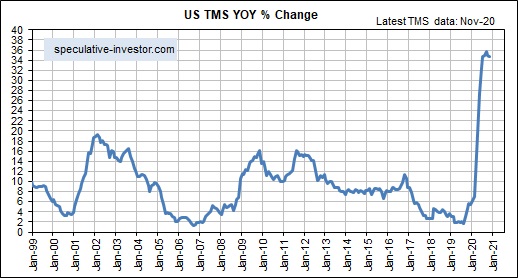

The following chart shows the year-over-year TMS growth rate (the monetary inflation rate) in the US. It has fallen sharply over the past 8 months — from around 11% to around 5% — and is now at its lowest level since 2008.

The chart displayed above suggests that the US economic boom* is on its last legs. It may well be, but the 2002-2006/7 boom continued for almost 2 years after the US monetary inflation rate fell to near its current level in early-2005.

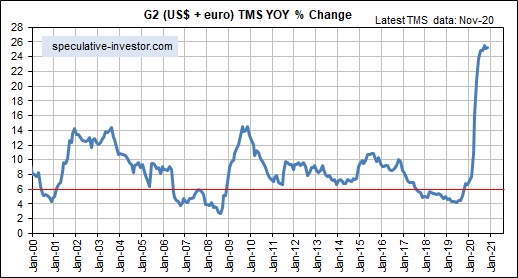

The reason for the long delay during 2005-2007 between the decline in the US TMS growth rate to a level that ordinarily would have ended the boom in less than 12 months and the actual ending of the boom was the offsetting effect of rapid monetary inflation in the euro-zone. This prompted me to develop a monetary aggregate that I call “G2 TMS”, which combines the US and euro-zone money supplies. Here is a monthly chart showing the growth rate of G2 TMS.

The rate of change in the G2 TMS growth rate has been the most useful leading indicator of the global boom-bust cycle over the past two decades. Of particular significance, a decline in the G2 TMS growth rate from well above 6% to below 6% warns of a shift from boom to bust within 12 months.

Related Posts

The Stock Whisper Of The Day: S, UNG, FCX, GM, USO

The Stock Whisper Of The Day: S, UNG, FCX, GM, USO EC

HH

2018 Comes Into Focus

EC

HH

2018 Comes Into Focus Buick Debuts China-Made Envision, Domestic Cars Going Overseas?

Buick Debuts China-Made Envision, Domestic Cars Going Overseas? EUR/USD Weakens Amid Global Economic Uncertainty And Strong US Dollar

EUR/USD Weakens Amid Global Economic Uncertainty And Strong US Dollar China Manufacturing Prices Decline 18th Month; China Hoping To Avoid Hard Landing

China Manufacturing Prices Decline 18th Month; China Hoping To Avoid Hard Landing Dividends By The Numbers Through January 2018

Dividends By The Numbers Through January 2018

Leave A Comment