Stock buybacks may be back as blackout session ends, but suddenly companies’ appetite to repurchase their own shares appears to be slowing sharply.

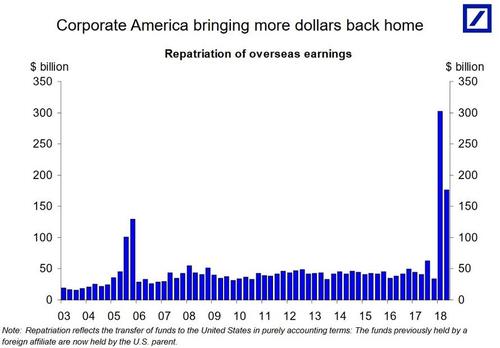

After an initial record surge in the amount of US corporate cash repatriated from offshore jurisdictions (if only for accounting purposes, as the bulk of said cash was already largely invested in domestic securities via offshore entities) following Trump’s tax law overhaul and tax repatriation holiday, the movement of foreign cash has slowed sharply.

This comes at a time when record notional corporate buybacks have not only surpassed total capex spending for the 2nd quarter in a row, but have been seen as responsible for the relentless bid supporting the stock market.

So why are offshore fund flow important?

Because, as many strategists have noted over the past year, with JPMorgan’s Nikolaos Panigirtzoglou doing so most recently in his latest Flows and Liquidity report over the weekend, US repatriation flows are a key leading indicator for US stock buybacks.

And the problem for stock market bulls, is that recent data are consistent with this idea that offshore cash repatriation is slowing considerably and by implication, so are buybacks.

The first piece of evidence cited by Panigirtzoglou is Q3 reporting season itself. The JPM strategist had argued previously that we can get a good idea of the amount of repatriated cash that has been actually deployed by looking at the earnings reports of US companies and in particular via observing the reduction in overall cash holdings. By simple elimination, when the offshore cash is repatriated but not deployed, then overall cash holdings should be unchanged as the only change that has happened is that a portion of cash has switched location from offshore to onshore. But when the repatriated cash is deployed – as has been the case with Apple for three consecutive quarters – in order for the company to buy back shares or to fund other activities, then the overall amount of reported cash holdings should decline.

Leave A Comment