US COMMERCIAL REAL ESTATE

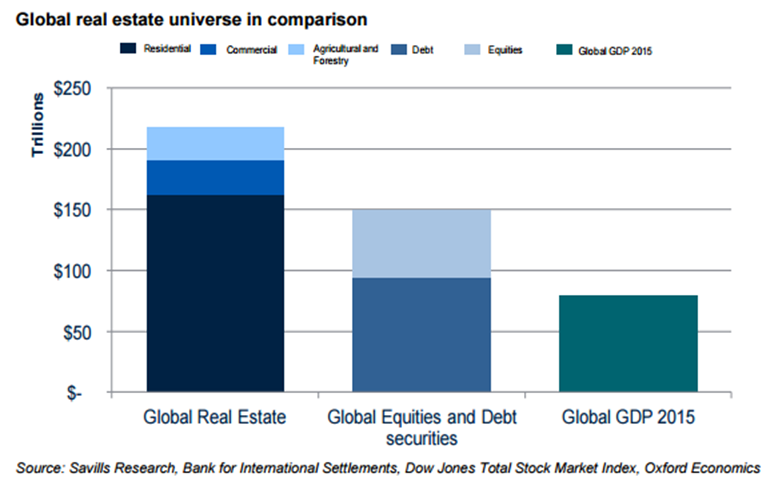

The Global Real Estate market dwarfs all financial markets by any comparison.

The Global Real Estate market being so large, it has always been stable and as such it is the favorite of institutions for long term investing – specifically Insurance companies, pensions, trusts endowments, small banks & credit unions etc. However, if it were to be destabilized only slightly it would have profound consequences globally, as well as in the US. The US Commercial Real Estate market presently approximates $13T or about one fifth the annual Global GDP.

A number of paradigms shifts currently underway and beginning to emerge could be just such catalysts.

The Us Commercial Real Estate market is so large it needs to be considered by sectors – Industrial, Office, Rental / Apartment and Retail. Through financing, regulations & codes, securitization products etc they are inexplicably linked. A shock wave in one will have consequences across the entire industry that can alter credit terms, financing availability, collateral requirements, rollover funding etc. In our new world of globalization, factors such as changes in foreign capital flows have a profound impact on any of the above variables.

Few may appreciate that the US is a dominate destination for such foreign capital.

Banking problems abroad, such as the EU which would require repatriation of capital, could impact prices and rollover financing quickly since commercial real estate is typically financed on 5 and 10 years terms so that supporting collateral values are maintained. This is a requirement because owners can and do simply “walk” away when they fail and collateral is the only protection for investors. The collateral being solely the value of the remaining real estate asset.

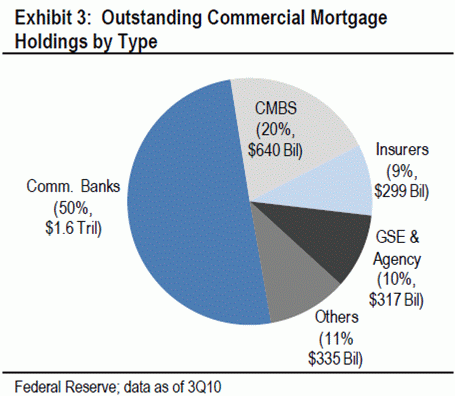

In the US,though banks are both financiers and owners, it is important to realize that the 8-12,000 small banks & credit unions along with Insurance companies, Pension Funds, Endowments, Trusts, Foundations etc are actually the ones “on the hook” for the bulk of US Commercial Real Estate.

WHAT COULD GO WRONG?

Because of the securitization complexity of the industry financed through MBSs, Leveraged Loans, Collateralized Loan Obligations, Synthetic CLOs etc., the risk exposures are immense. The US housing industry imploded via comparably simple securitization product structures such as CDS’s, CDO and ABSs. Few professionals would claim they have a grasp or understanding of all the creative and secretive means used to finance these modern multi-billion dollar commercial real estate projects. These projects are based on underlying assumptions of growth, rates, prices, sustained trends etc..

Leave A Comment