Secular bears are born from extended periods of indiscriminate buying and speculation that drive prices paid for securities to irrational multiples of real-world items like revenues, cyclically adjusted earnings, tangible assets and wages. And then they mean revert.

Bulls say buying and holding at any price is smart investing, because ‘over the long-run’ market cycles spend more time and points going up than down. This misses the math of the matter utterly.

It is not the duration of the upcycle that is definitive of net returns, but rather exposure to the intermittent loss cycles.

The inset table on the far right of the below chart from Lance Roberts shows the bull and bear periods for the S&P 500 since 1900–both in terms of index points and the percentage gained and lost each time. As shown in the chart itself, the shorter recurring bear cycles take back most and sometimes all of the real gains clocked during the longer bull upcycle.

In addition, and most importantly, since bull markets increase confidence and risk-taking as they go, capital tends to get pushed in most near tops and least near bottoms, making the cyclical mean reversion periods much more capital destructive than even this chart would suggest.

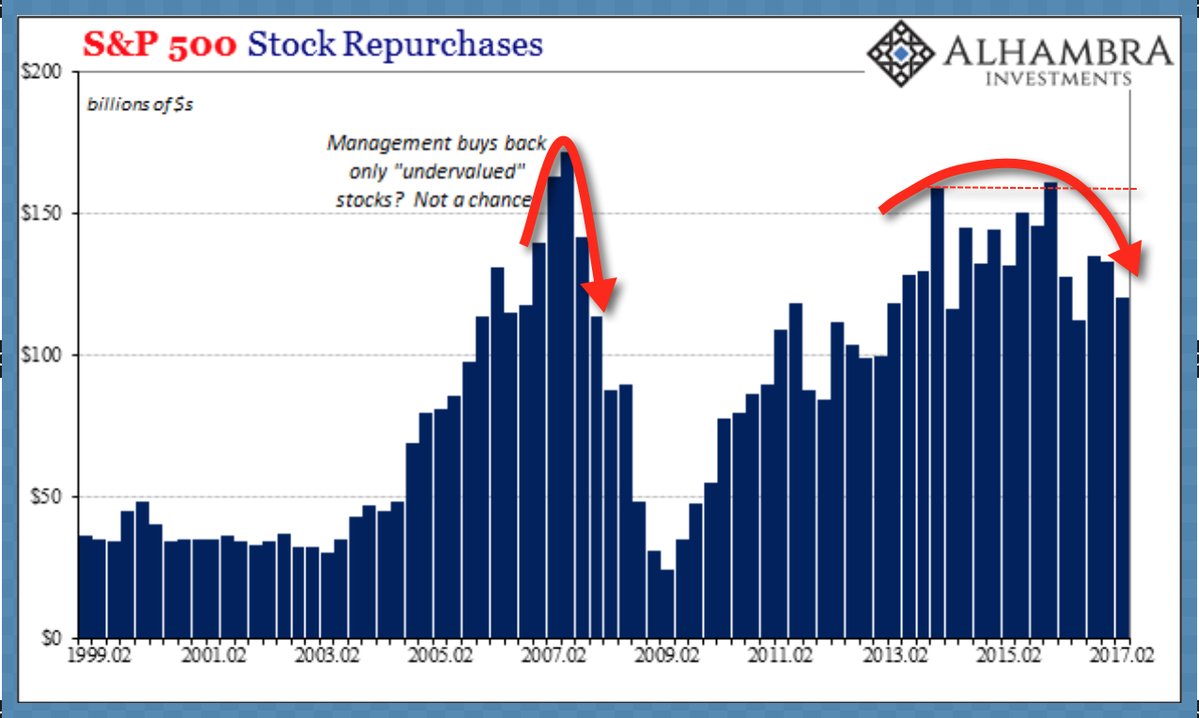

The same goes for corporate management teams and their so-called “active” shareholders, that infamously waste good money buying back badly over-valued stocks each market peak, as shown here since 1999.

As people amass more and more of their life savings and have less and less time to grow back losses, the extent to which they are protected from the downcycles becomes the most defining element of real-life investment outcomes. This is especially the case during secular bear periods, where the recurring cyclical declines tend to be twice as deep and long as during periods starting from low valuations (ie., secular bulls like 1982-2000).

Related Posts

What’s The Real Value Of Your Stock?

What’s The Real Value Of Your Stock?- EU: Ireland Must Recover Unpaid Taxes From Apple Of Up To EUR13B, Plus Interest

EIA Data Keeps Natural Gas On The Floor

EIA Data Keeps Natural Gas On The Floor Crypto has recovered from China’s FUD over a dozen times in the last 12 years

Crypto has recovered from China’s FUD over a dozen times in the last 12 years- S&P 500 To Set New Records: Ride High With These ETFs

- Most Active Stock Options For End Of Day April 17, 2017 – BAC, WFT, ILG, AAPL, AMD

Leave A Comment