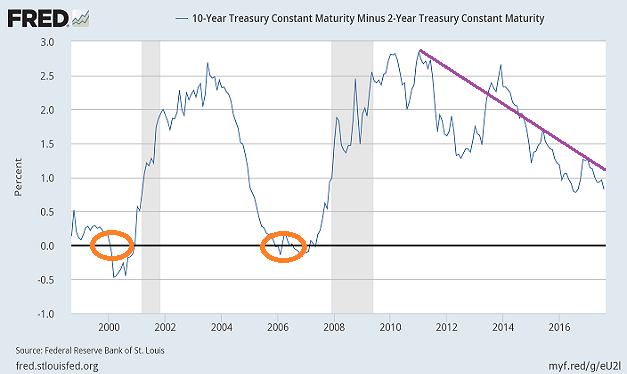

In the current business cycle, the Treasury bond yield curve has rarely been flatter. The spread between 30s and 2s is a paltry 1.4% and the spread between 10s and 2s is a meager 0.8%.

Historically, the yield curve has been close to flawless as an expansion-contraction indicator. When a flattening curve dipped below ‘zero,’ the inversion foreshadowed seven out of the last 8 recessions.

However, the Federal Reserve’s creation of trillions in electronic dollar credits (a.k.a. “quantitative easing” or “QE”) alongside lengthy near-zero rate policy altered the predictive capability of the yield curve. For instance, the Fed has more recently bumped overnight lending rates up to 1%-1.25% on the shortest end. Yet economic and geopolitical uncertainty have been pressuring longer-term yields and sending them downward. Still, with shorter-term rates so low from the get-go, there may not be a hallowed moment when the spread between 10s and 2s hit 0% and subsequently usher in a recessionary environment.

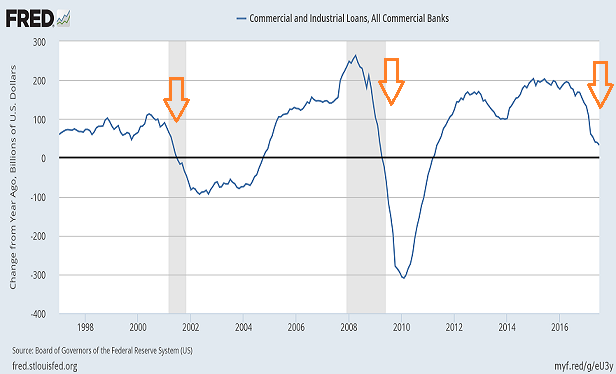

On the flip side, few would declare that the flattening of the yield curve is signaling strength. It hurts bank profitability. Worse, it inhibits their willingness to lend. Business loans have been sinking in dramatic fashion.

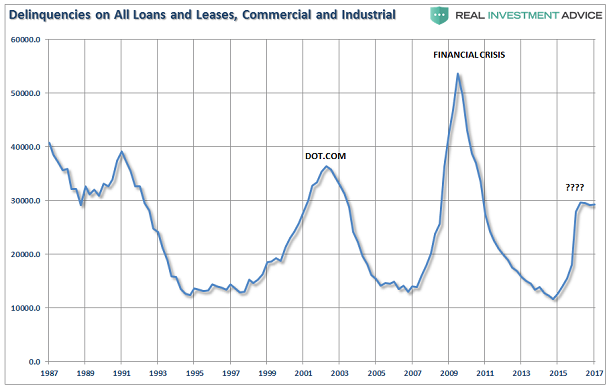

Granted, a great deal of trouble may be concentrated in the beleaguered retail and energy sectors. Nevertheless, it certainly cannot be helpful that delinquencies are climbing.

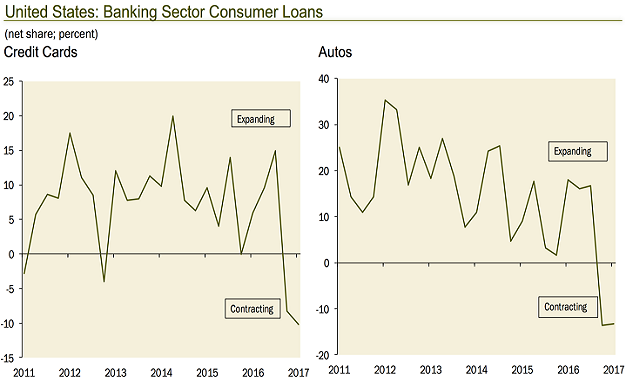

If commercial and industrial loans (C&I) are stalling, perhaps the ‘confident’ consumer is picking up the slack. Not really. Credit cards and auto loans have been declining as well.

Keep in mind, the central bank of the United States (a.k.a. “the Fed”) has not been genuinely concerned with its dual mandate of full employment and stable inflation. Since 2009, monetary policy leaders have been hell-bent on getting the investment community to remove their dollars from cash accounts and place them in assets like stocks, bonds and real estate. Prices on most market-based assets continue to hover near all-time highs with no regard for traditional valuation or credit cycle deterioration.

Related Posts

Dogecoin community donates $53K to Ukraine as country hints at upcoming airdrop

Dogecoin community donates $53K to Ukraine as country hints at upcoming airdrop- Silver Price About To Turn Bullish For 2017 And 2018

Small Cap Stocks Update: Russell-2K All Good Under The Hood

Small Cap Stocks Update: Russell-2K All Good Under The Hood Market Commentary: SP500 Continues To Climb As Other Averages Trade Sideways

Market Commentary: SP500 Continues To Climb As Other Averages Trade Sideways Watch The Forty

Watch The Forty A Good Employment Report, But With Risks

A Good Employment Report, But With Risks

Leave A Comment