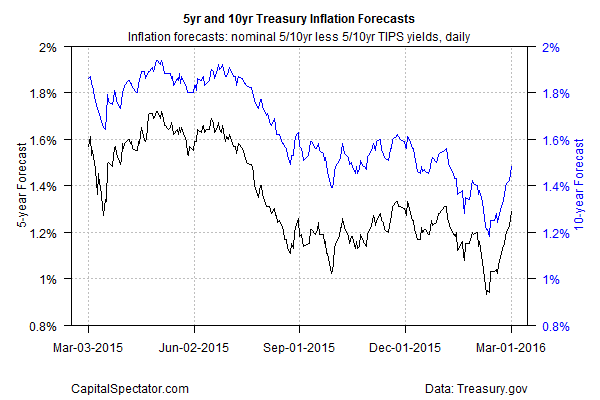

The US Treasury market’s implied inflation forecast has surged in recent days, albeit after reaching unusually low levels last month. Nonetheless, the roller-coaster of revising expectations rolls on, and this time there’s an upside bias bubbling. The spread between the nominal 10-year yield and its inflation-indexed counterpart reached 1.48% yesterday (Mar. 1), based on daily data from Treasury.gov. That’s still a low rate relative to the roughly 1.5%-2.5% range in recent years. But the latest pop marks a sharp increase from mid-February, when the market’s inflation forecast at one point dipped to 1.18%.

The upward bias of late looks reasonable in the wake of last week’s January reporton personal income and spending, which revealed a firmer inflation trend. The personal consumption expenditures (PCE) price index increased 1.3% for the year through January, the strongest annual gain since Oct. 2014. Meanwhile, the Fed’s preferred inflation benchmark—core PCE, which excludes food and energy—ticked up to a 1.7% year-over-year increase, which marks the biggest advance since July 2014.

The upward repricing of inflation expectations can be seen as a correction after weeks of anticipating weaker economic growth via bearish signals pouring forth from the equity and bond markets. But the January macro profile suggests that the US macro trend is stronger than the previously assumed. Slow growth continues to be the working assumption for the near-term future, but the case is still unconvincing for arguing that a new recession has started, or is about to start. Indeed, the Atlanta Fed’s GDPNow model is currently projecting a 1.9% gain (seasonally adjusted annual rate) for US output in this year’s first quarter (as of Mar. 1). That’s a modest increase, but it’s conspicuously above the 1.0% GDP rise for last year’s fourth quarter.

Perhaps, then, it’s no surprise that the market is again repricing yields to reflect expectations for a modest growth trend. The 2-year Treasury yield, which is considered the most sensitive to rate expectations, has rebounded to 0.85% as of yesterday (Mar. 1)—the highest since late-January.

Related Posts

Is Bitcoin bullish or nah? Here is what is really going on with BTC price

Is Bitcoin bullish or nah? Here is what is really going on with BTC price Dollar Softens Ahead Of Start Of FOMC Meeting

Dollar Softens Ahead Of Start Of FOMC Meeting Billion Dollar Unicorns: Souq.com The Middle East Entry To The Club

Billion Dollar Unicorns: Souq.com The Middle East Entry To The Club How The Investor Fundamentally Changed The Silver Market

How The Investor Fundamentally Changed The Silver Market Gold Extends Losses As U.S. Stocks Rally

Gold Extends Losses As U.S. Stocks Rally- Economic Data And Forecasts For The Weeks Of November 20 And November 27

Leave A Comment