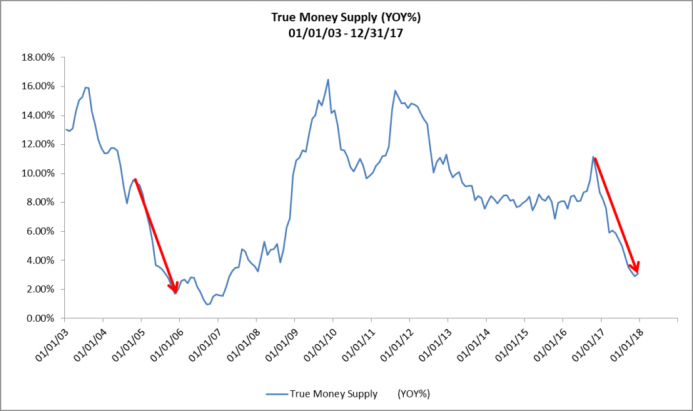

Jeffrey Peshut at RealForecasts.com has composed several very illuminating graphs based on the Rothbard-Salerno True Money Supply (TMS). In one graph Peshut shows the collapse of the growth rate of TMS beginning at the end of 2016, which was caused by the Fed beginning to raise the fed funds target rate at the end of the preceding year. What is of great interest is that the recent deceleration of monetary growth (the second red arrow) almost exactly matches in extent and rapidity the monetary deceleration (the first red arrow) that immediately preceded the financial crisis of 2007-2008.

The Fed recently reaffirmed its commitment to increasing the fed funds rate three more times in 2018 and has just begun its program of shrinking it balance sheet by a cumulative total of $450 billion by the end of 2018. Given these circumstances, I am inclined to agree with Peshut’s conclusion:

“it’s easy to see that the growth of TMS could grind to a halt and even begin to contract later this year.”

With equity prices heading back toward historic highs after the January “correction” and housing prices bubbling to an all time high in major markets, the suppression of the TMS growth rate, if it is sustained for the rest of the year, portends another credit crisis and housing bust, followed by an economic recession for the U.S. economy. As Peshut’s graph below indicates the qualitative relationship between TMS growth, credit crisis, and recession has been remarkably clear since 1978. Of course, this empirical relationship should not surprise us, because it is nothing but an illustration of the Austrian theory of the business cycle.

Related Posts

Crypto more popular among millennials than mutual funds, survey shows

Crypto more popular among millennials than mutual funds, survey shows Euro To Parity And Beyond

Euro To Parity And Beyond Does The Model X Ramp Spell Long Term Trouble For Tesla?

Does The Model X Ramp Spell Long Term Trouble For Tesla? Brazil Releases Shocking GDP “Obituary”: “It’s Mutated Into An Outright Depression,” Goldman Exclaims

Brazil Releases Shocking GDP “Obituary”: “It’s Mutated Into An Outright Depression,” Goldman Exclaims Will It Be Unlucky Friday The 13th For US Retail Sales

Will It Be Unlucky Friday The 13th For US Retail Sales EOS Bullish Momentum In Wait For A Breakout

EOS Bullish Momentum In Wait For A Breakout

Leave A Comment