A Curious Collapse

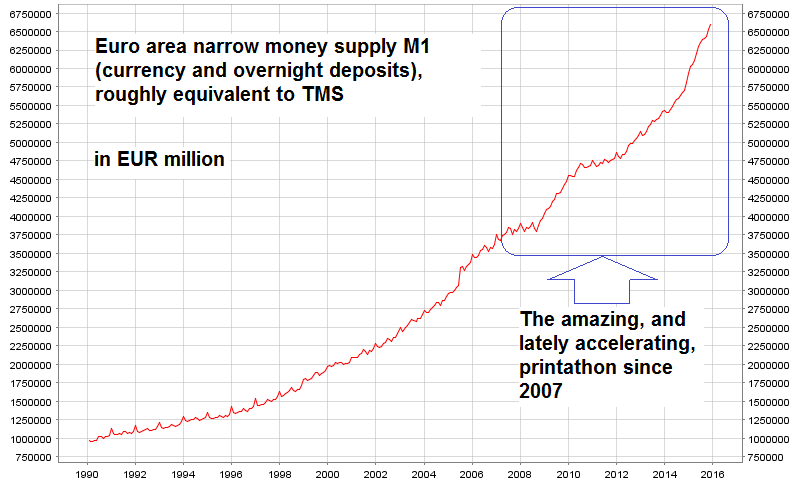

Ever since the ECB has begun to implement its assorted money printing programs in recent years – lately culminating in an outright QE program involving government bonds, agency bonds, ABS and covered bonds – bank reserves and the euro area money supply have soared. Bank reserves deposited with the central bank can be seen as equivalent to the cash assets of banks. The greater the proportion of such reserves (plus vault cash) relative to their outstanding deposit liabilities, the more of the outstanding deposit money is in fact represented by “covered” money substitutes as opposed to fiduciary media.

Euro area true money supply (excl. deposits held by non-residents) – the action since 2007-2008 largely reflects the ECB’s money printing efforts, as private banks have barely expanded credit on a euro area-wide basis since then.

Many funny tricks have been employed to keep euro area banks and governments afloat during the sovereign debt crisis. Essentially these consisted of a version of Worldcom propping up Enron, with the central bank’s printing press as a go-between.

As an example here is how Italian banks and the Italian government are helping each other in pretending that they are more solvent than they really are: the banks buy government properties (everything from office buildings to military barracks) from the government, and pay for them with government bonds. The government then leases the buildings back from the banks, and the banks turn the properties into asset backed securities. The Italian government then slaps a “guarantee” on these securities, which makes them eligible for repo with the ECB. The banks then repo these ABS with the ECB and take the proceeds to buy more Italian government bonds – and back to step one. Simply put, this is a Ponzi scheme of gargantuan proportions.

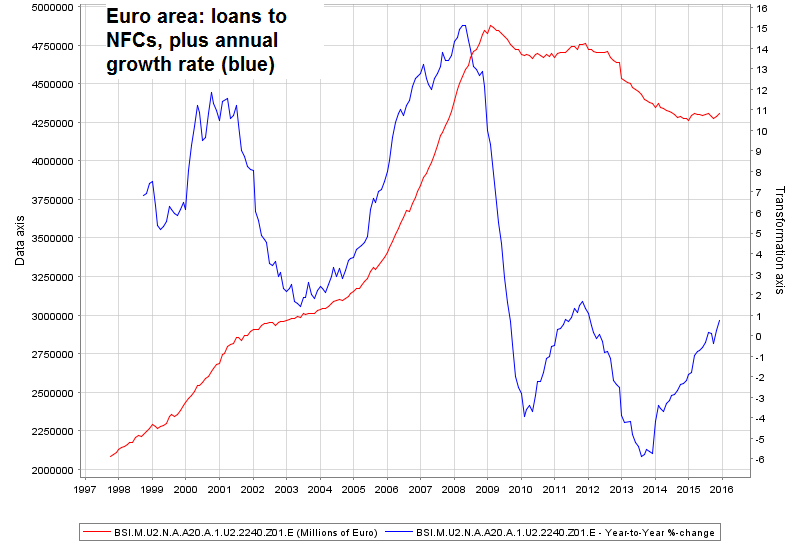

Still, in view of these concerted efforts to reliquefy the banking system, one would expect that European banks should be at least temporarily solvent, more or less. Since they have barely expanded credit to the private sector, preferring instead to invest in government bonds, the markets should in theory have little to worry about.

Euro area bank loans to non-financial corporations, with annual growth rate (blue line).

In fact, on account of new capital regulations, European banks are almost forced to amass government securities – as government bonds have been declared to represent “risk-free” assets, which reveals an astounding degree of chutzpa on the part of European authorities in the wake of the sovereign debt crisis.

This makes one wonder why the Euro Stoxx Bank Index suddenly looks like this:

Related Posts

Chinese Bonds Are Crashing, What It Means For The Economy

Chinese Bonds Are Crashing, What It Means For The Economy Investors eye T’s & C’s

Investors eye T’s & C’s The Power Of Price Spikes On Intraday Charts

The Power Of Price Spikes On Intraday Charts AUDUSD Analysis & AUDUSD Price Prediction Forecast – Saturday, May 18

AUDUSD Analysis & AUDUSD Price Prediction Forecast – Saturday, May 18 EC

Industry Disruption Is Creating A Minefield Of Value Traps For Investors

EC

Industry Disruption Is Creating A Minefield Of Value Traps For Investors Irish Border And Magical Realism

Irish Border And Magical Realism

Leave A Comment