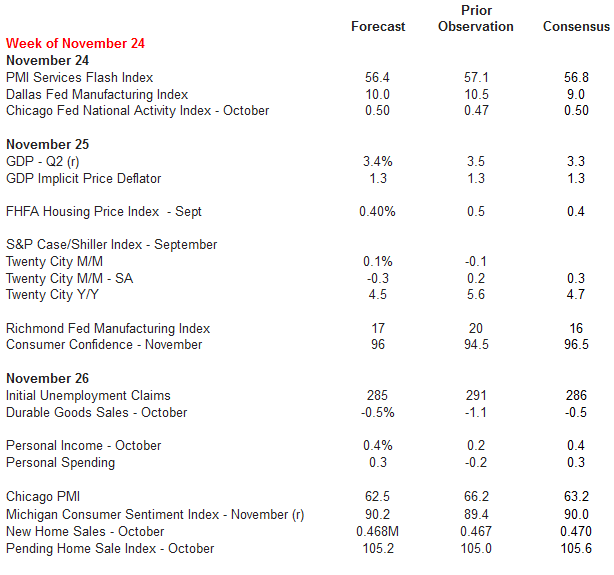

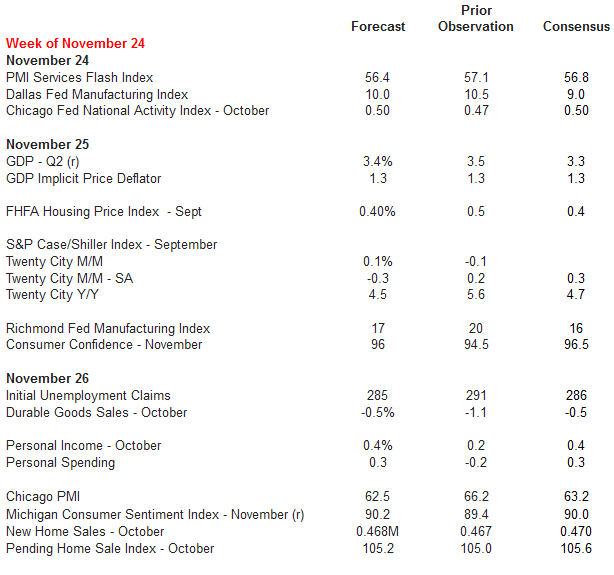

This week markets will focus on the revised GDP report, which the consensus shows falling a bit from last month’s flash estimate of 3.5 percent. Potentially upsetting markets, the consensus expects durable goods orders fell 0.5 percent in October; however, that would be mostly adjustments in the volatile transportation sector—dominated by the lumpiness in aircraft sales.

What should have market analysts’ attention—and likely will not—is the stealth story in the Case-Shiller housing price report. For this most reliable of housing market indicators, the press likes to focus on the year-over-year figure, which should remain positive someplace between 4.4 to 4.8 percent— thanks mostly to good numbers during the earlier month of the trailing period. However, non-seasonally adjusted monthly data has been falling the last four months running.

Another negative or near zero positive number in the observed value for monthly price changes indicates the housing price recovery is done. That is not a bad thing, as long as prices don’t reverse direction too much in face of higher mortgage rates. Housing values may not be at their pre-crisis zenith, but those were unrealistic anyway.

Affordability and steady prices will do much more for the overall economic recovery by stimulating: young folks to finally get out and buy new houses, the housing industry to get serious about affordability and quit its obsession with McMansions, and the building materials, appliance and other supplying industries.

…and what everyone seems to care most about

As for the stock market, stay focused on the medium-term prize—the bull run isn’t over. With quantitative easing in China, Japan and coming soon in Europe, the S&P could easily run all the way to 2500 before the party is done.

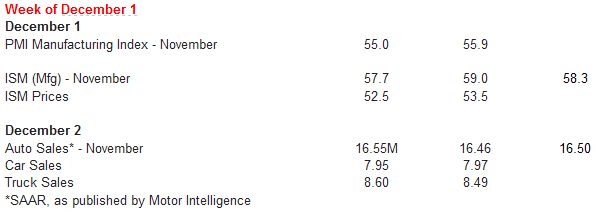

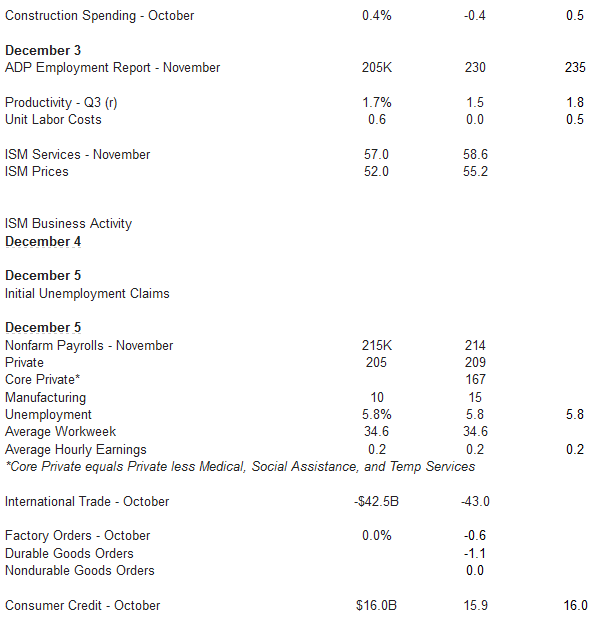

Here are my forecasts for upcoming economic data.

Related Posts

Global Trade Just Snapped: Container Freight Rates Plummet 70% In 3 Weeks

Global Trade Just Snapped: Container Freight Rates Plummet 70% In 3 Weeks Sea Of Red: Crypto Carnage Continues As Bitcoin Rebound Stalls

Sea Of Red: Crypto Carnage Continues As Bitcoin Rebound Stalls EUR/USD Forecast Jan. 29 – Feb. 2 2018

EUR/USD Forecast Jan. 29 – Feb. 2 2018 Can Fossil Jumpstart Strong Earnings With Smart Accessories?

Can Fossil Jumpstart Strong Earnings With Smart Accessories? The Fed Is A Huge Driver In Kyle Bass China Currency Short

The Fed Is A Huge Driver In Kyle Bass China Currency Short The Canadian Dollar Rose On Friday After Positive Job Data

The Canadian Dollar Rose On Friday After Positive Job Data

Leave A Comment