Two points from the 2018Q2 2nd release: GDO is smoother, and a breakout has not yet appeared.

First, consider real GDP and real GDO (average of GDP and GDI) growth, q/q SAAR.

Figure 1: Real GDP growth (blue), and real GDO growth (red), both q/q SAAR, in log terms. Light orange shading denotes Trump administration. Source: BEA, 2018Q2 2nd release, and author’s calculations.

While the quarter-on-quarter GDP growth is high, it’s not unparalleled (see discussion in this post). In addition, GDO, which has shown itself to be a better predictor of revised values of GDP, indicates less rapid growth (see Justin Fox’s article today).

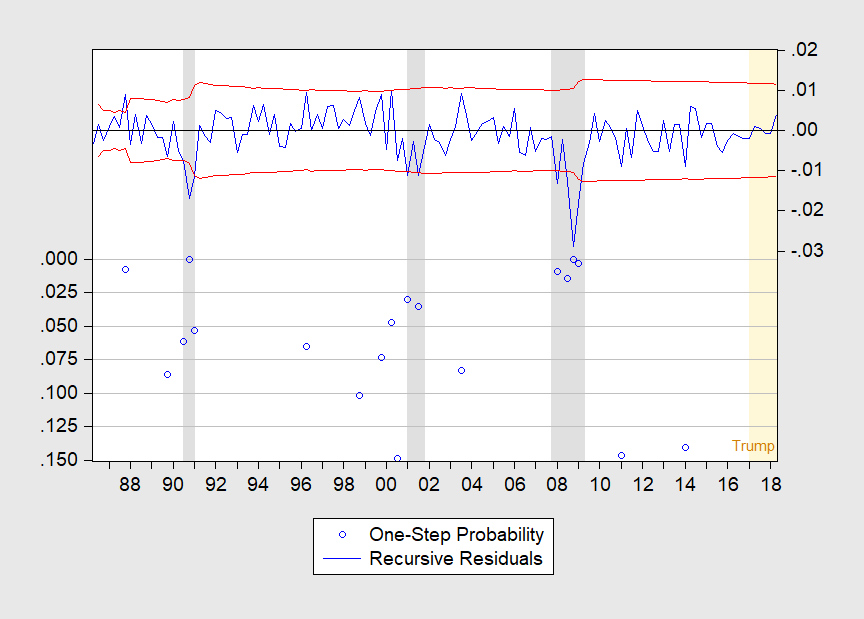

Second, returning to GDP, is there evidence of a breakout in growth? Consider recursive one-step-ahead regression residuals. OLS regressions ?yt = const are estimated recursively (i.e., the sample is progressively augmented after a starting sample) over the Great Moderation period, 1986-2018, and a test applied to see if the residual from the one-step-ahead forecast looks like it comes from a different distribution (the null hypothesis is same distribution).

Figure 2: Recursive one-step-ahead residuals (blue, right scale). P-values (blue circles, left scale). Light orange shading denotes Trump administration. Source: BEA, 2018Q2 2nd release, and author’s calculations.

As indicated in the graph, no break occurs after the Great Recession. These results are robust to another specification (ARIMA(1,1,0)), except a structural break is found in early 2014 (at the 10% msl).

I will say I won’t be surprised to see breaks in the future, particularly with volatility in the net export series likely due to both trade measures and the accounting effects of the TCJA.

Related Posts

Nordstrom Reports Strong Q3 Earnings, Updates Outlook

Nordstrom Reports Strong Q3 Earnings, Updates Outlook E

Markets Weekend Update – March 12, 2016

E

Markets Weekend Update – March 12, 2016- The U.S. Equity Market Chart Book

Coinbase to invest in Indian crypto and Web3 amid tax regulation clarity

Coinbase to invest in Indian crypto and Web3 amid tax regulation clarity- Fed Opens Negative Interest Rate Pandora’s Box: What Happens Next

JP Morgan – Heavy Accumulation Of Precious Metals In April

JP Morgan – Heavy Accumulation Of Precious Metals In April

Leave A Comment