I sincerely hope everyone who’s still plowing money into corporate credit has a good handle on what it is they’re doing because investment grade corporate debt issuance is running at a record pace, and just topped $1 trillion faster than any year in history.

This is six straight years of $1 trillion plus in the supply and needless to say, it’s being supercharged by companies trying to get out ahead of what they assume will be a more aggressive Fed down the road.

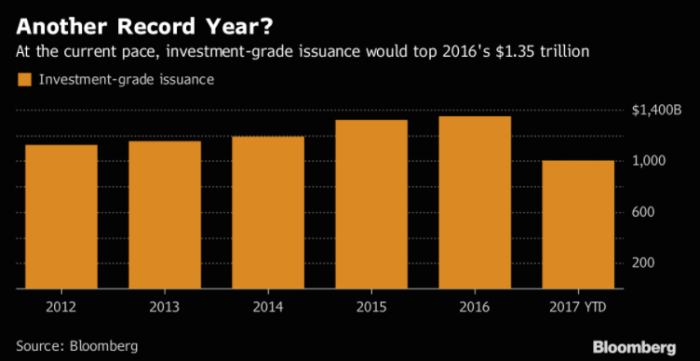

As you can see from the subheader on that chart, if we keep going at the current rate, 2017 will top 2016 which topped 2015 which topped 2014 and on and on.

This is all the same old QE-driven supply-demand picture.

Part of this is probably foreign investors running away screaming from NIRP economies in search of any semblance of yield. US corporates are more than happy to oblige. They’re also happy to plow some of the proceeds from these sales into EPS-inflating buybacks, a move that helps to levitate benchmarks which in turn improves the optics around the stock market from the perspective of retail investors, and around the bubble machine we go.

Here’s Bloomberg from a piece out yesterday:

After years of the central bank stimulus, signs of froth are everywhere. On the debt side, U.S. high-grade companies have already sold about $1 trillion of bonds this year, and are on track to break last year’s issuance record. Junk bond yields, at just 5.8 percent, are near all-time lows. In stocks, U.S. markets are close to record highs.

The Fed hasn’t been buying corporate debt, but as it snapped up Treasuries and mortgage securities, bond yields broadly fell, making it cheaper for companies to borrow. Corporations have often used the money they raised to buy back shares, buoying the stock market. That’s what worries a group of investors and banks known as the Treasury Borrowing Advisory Committee, which counsels the government on its funding and the economy.

“The private sector piggy-backed on the Fed’s large-scale asset purchases, a move that promoted a surge in corporate borrowing and tighter risk spreads,” wrote Jason Cummins, TBAC chairman, in an Aug. 2 letter to Treasury Secretary Steven Mnuchin. Cummins is head of research at hedge fund Brevan Howard.

Leave A Comment