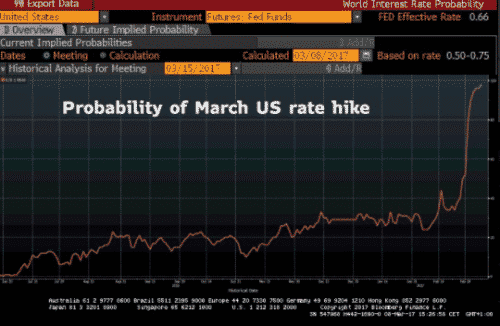

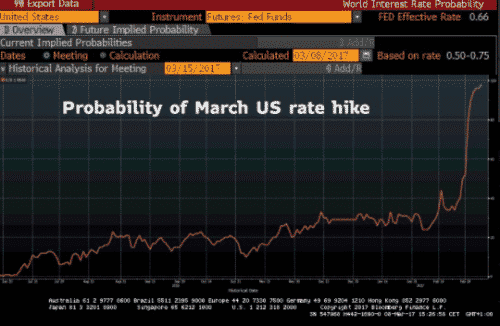

Tomorrow, the BLS will release the February jobs numbers for the US economy. This is the last piece of major US economic data before the Fed meets next week to decide on US monetary policy. All indications are that the number will be good. The ADP employment report released yesterday showed 298,000 private sector jobs added to the economy, the best showing in some 11 years. And January’s report showed non-farm payrolls rising by 227,000.

Economists are only expecting 195,000 jobs added tomorrow. That’s an easy number to beat. And so the Fed is almost certain to raise interest rates unless something dramatically bad comes out. And even then, the Fed could hike, pegging the data as a one-off. That’s what the market thinks.

Why this matters: right now, the Fed is in a tightening phase. The question on everyone’s mind is whether the Fed is behind the curve or is getting ahead of itself. For example, the latest numbers out of the Atlanta Fed’s GDPNow model show the economy growing at a 1.2% pace this quarter. That figure shows a decelerating economy, with Q4 lower than Q3 and this quarter even lower, not an accelerating one.

Nevertheless, if the numbers are good, not only will the Fed raise rates, the prospect of another hike in May would rise too. And that is bullish for the US dollar and bearish for US bonds. US 2-year rates are already at the highest levels in 17 years relative to the German 2-year.

It’s not inconceivable that the Fed hikes more than three times this year, given how the Fed has started to position policy. Further monetary policy divergence will only exacerbate the differential between Treasuries and German Bunds though. With US Commerce Secretary Wilbur Ross recently saying on CNBC that, “It’s not that the dollar is too strong, it’s that some of the other currencies are weaker than they should be,” we could see major tension between the US and its trading partners.

Related Posts

5 Must-See Economic Charts Show Why Stocks May Stumble In 2016

5 Must-See Economic Charts Show Why Stocks May Stumble In 2016 US Dollar Strengthens

US Dollar Strengthens- Privacy coins are surging. Will regulatory pressure stall their stellar run?

- Why Gold Is A Sure Thing In 2017 (SPONSORED POST)

Yen Rally Nearly Done

Yen Rally Nearly Done September 2015 Economic Forecast: Some Improvement Over Last Month’s Terrible Forecast

September 2015 Economic Forecast: Some Improvement Over Last Month’s Terrible Forecast

Leave A Comment