And we’re back!

The Dow is up 75 points pre-market, back at 26,700 and the Nasdaq is testing the 7,600 line, which will certainly be bullish if they break over it but, until then, I like /NQ as a short with tight stops above. We also re-shorted Oil (/CL) Futures at $72.50 this morning – also with tight stops above as it sets a nice, positive risk/reward ratio to do so. We made $500 shorting /CL yesterday on a 0.50 drop and about the same on Gasoline (/RB) as it fell so no reason not to give them another chance to make us money, right?

Trade Wars are not good for oil demand and 74 out of 98 S&P Companies that have issued Q3 guidance so far have issued negative guidance and that’s already the worst rate since Q1 of 2016 when the S&P fell 15% from 2,100 to 1,800 as earnings rolled over. It’s still early in the cycle but negatives outpacing positives 3:1 is certainly something we should be taking note of. Or, we can add it to the ever-growing list of negatives that investors are ignoring in this rally…

Insight/2018/09.2018/09.21.2018_EI/Percentage%20of%20Companies%20Issuing%20Negative%20EPS%20Guidance.png?t=1537864669380&width=910&name=Percentage%20of%20Companies%20Issuing%20Negative%20EPS%20Guidance.png)

Keep in mind that figure is WITH all the buybacks and WITH all the M&A activity and WITH the still-low interest rates and WITH what is still $60Bn/month in QE, though that may change on Wednesday if the Fed begins to pull back – as it has said it was planning to do.

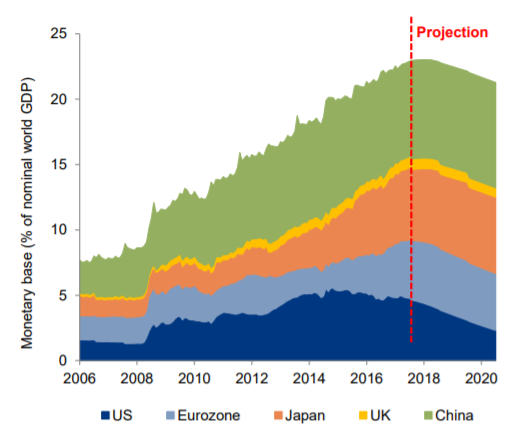

Though our Fed has begun to somewhat unwind their QE program, the rest of the World’s QE is only just now hitting its peak, so of course the markets are at record highs when there are record amounts of money chasing equities but this (2018) should mark the end of the Global Liquidity Boom and now comes the reduction – a slow and painful process that will be with us for years as the Central Banksters race to drain the monetary swamp before all those Dollars lying around begin to turn inflationary.

This is the greater market picture you need to be concerned with – it’s the macro that will be driving the market for years to come – especially as the Central Banks, so far, have taken only the smallest of baby steps to begin unwinding a decade of QE programs that have flooded the markets with liquidity and kept interest rates artificially low. As you can see from the next chart – we’re still a year away from actually withdrawing stimulus but the entire World turns net negative in about the middle of next year:

Leave A Comment