from the New York Fed

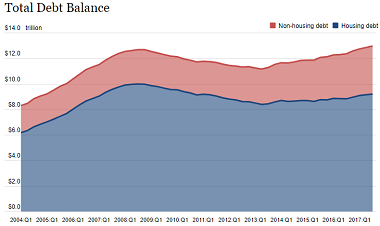

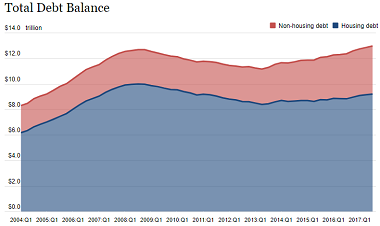

The Federal Reserve Bank of New York’s Center for Microeconomic Data today issued its Quarterly Report on Household Debt and Credit, which reported that total household debt increased by $116 billion (0.9%) to $12.96 trillion in the third quarter of 2017. There were increases in mortgage, student, auto and credit card debt (increasing by 0.6%, 1.0%, 1.9% and 3.1% respectively) and a modest decline in home equity lines of credit (HELOC) balances (decreasing by 0.9%).

The Report is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample of individual- and household-level debt and credit records drawn from anonymized Equifax credit data.

Credit card and auto loan flows into delinquency increased. Specifically, credit card flows into delinquency have increased over the past year, while auto loan flows into delinquency have been steadily increasing for several years. Also notable, auto loan originations were at $150.6 billion, up slightly from the previous quarter, marking the second highest level in more than a decade. The New York Fed also issued an accompanying blog post which examines the changes in the auto loan market in terms of originations and performance by lender type.

“Delinquency flows across several debt types climbed this quarter, including for auto loans,” said Wilbert van der Klaauw, senior vice president at the New York Fed. “Examining the auto loan market more closely revealed notable differences between auto finance and auto bank lenders. Delinquency rates among auto finance lenders are considerably higher and rising, especially for subprime borrowers, in part reflecting differences in underwriting standards.”

The Report includes a one-page summary of key takeaways and their supporting data points. Overarching trends from the Report’s summary include:

Housing Debt

Related Posts

The Inevitable Crash – Part 1

The Inevitable Crash – Part 1 Euro-zone Inflation Hits 0.5%, GDP 0.3%, As Expected

Euro-zone Inflation Hits 0.5%, GDP 0.3%, As Expected AstraZeneca Enters Agreement With Grunenthal To Divest Rights To Zomig

AstraZeneca Enters Agreement With Grunenthal To Divest Rights To Zomig Fastest S&P 500 Correction Since 1928?

Fastest S&P 500 Correction Since 1928?- GBP/USD Tumbles As Internal Politics Take Over From External Politics

ISIS Unveils Its New Gold-Backed Currency To Remove Itself From “The Oppressors’ Money System”

ISIS Unveils Its New Gold-Backed Currency To Remove Itself From “The Oppressors’ Money System”

Leave A Comment